Zero Emissions in the UK by 2050?

Some elaborate window dressing from the UK Government...

In June 2019, the UK Government announced that it was binding the UK to zero Greenhouse gas (GHG) emissions by 2050. According to a statement by the Government the UK will be the first global economy to pass such ambitious legislation.

Apparently the UK has ‘reduced emissions by 42% while growing the economy by 72%’ and that ‘clean growth’ is ‘at the heart of our modern Industrial Strategy.’ The announcement goes on to say that such reductions will be met by offsetting schemes and by technological solutions such as carbon capture and storage (CCS). The question is — is this just window dressing or genuine Government policy? Closer examination of the announcement suggests the former, possibly as a reaction to the rise of climate awareness through activities from Extinction Rebellion and the youth strikes that has been manifesting across the country. The notion that UK emissions have reduced by 42%, ignores the fact that much of those emissions have been emitted elsewhere.

Research conducted by the University of Leeds Sustainability Research Institute demonstrates this. The convention is for countries to report emissions from within borders. But this does not account for consumption based emissions, which includes imported and exported goods. It is noted that, ‘Consumption-based emissions do not have to be reported officially by any country’, but emphasises that, ‘This model is important as it challenges the conventional reporting of carbon emissions.’

As part of the remit within the United Nations Framework Convention on Climate Change (UNFCCC), countries, including the UK, are required to submit annual emission inventories based on “territorial-based emission inventories”:

This method of reporting is limited since it accounts for emissions within the UK but excludes emissions emitted in international territory.

The following graph illustrates the position:

This generates an obvious disparity thus masking the real impacts of consumption emissions.

It’s difficult to work out where the growth figure of 72% for the UK economy came from. According to Full Fact, the UK economy was recently lagging behind the G7 (Canada, France, Germany, Italy, Japan, US along with the UK). As the following graph shows, there was a relatively quick recovery from the initial impact of the financial crash of 2008. Since then growth has fluctuated, with a dip setting in following the period after the Brexit referendum.

There is no context to the figure quoted by the Government. As such it is essentially meaningless. As Full Fact puts it:

Simply quoting figures on growth won’t tell the full story. Full Fact wants to see greater accountability for public figures who mislead us.

Then there’s the statement that the Government ‘has put clean growth at the heart of our modern Industrial Strategy.’ This contradicts a record of slashing investment in renewable energy and a persistent push on fracking. As Renewable UK reported in 2015, fossil fuels were receiving subsidies to the tune of £26 Billion, whilst support for renewables was cut. This was based on data from the IMF. By comparison:

The cost of supporting all renewable energy technologies in 2014/15 is £3.5 billion according to figures from the Department of Energy and Climate Change.

Another casualty was the feed in tariff scheme, which ended in 2019, following a prior Government announcement. This was set up in 2010, allowing owners of small scale renewable generators to be paid a fixed price for selling excess power to the grid.

The push on fracking across the UK continues. Fracking company Cuadrilla Resources continues its efforts to drill in Lancashire in the hope of actually achieving hassle free operations, despite evidence to the contrary.

The Government announcement then goes on to detail how it intends to achieve zero emissions by 2050. It states:

Net zero means any emissions would be balanced by schemes to offset an equivalent amount of greenhouse gases from the atmosphere, such as planting trees or using technology like carbon capture and storage.

Firstly, planting trees isn’t going to make any impact on emissions within 30 years. This has been borne out by a study published in 2017 by the Journal Earth’s Future. This is the basic summary of the research:

First, we show that biomass plantations with subsequent carbon immobilization are likely unable to “repair” insufficient emission reduction policies without compromising food production and biosphere functioning due to its space‐consuming properties. Second, the requirements for a strong mitigation scenario staying below the 2°C target would require a combination of high irrigation water input and development of highly effective carbon process chains. Although we find that this strategy of sequestering carbon is not a viable alternative to aggressive emission reductions, it could still support mitigation efforts if sustainably managed.

In short, attempting to mitigate CO2 emissions through biomass planting would require huge tracks of land, which would impact food production ‘with intolerably large environmental and social costs.’ Huge quantities of water would be required for irrigation, which could be problematic. Considerable nitrogen fertiliser use would also be required, a process that itself has high GHG emissions. Planting trees therefore simply isn’t a viable long term solution on a large scale, especially whilst there are areas of the planet that are still vulnerable to deforestation.

Secondly there’s carbon capture and storage (CCS), a technology that is untested on a large scale. This article from the Carbon Tracker Initiative outlines the pros and cons. The message is that ‘CCS is not a substitute for using less fossil fuels’.

Further research from the Massachusetts Institute of Technology has demonstrated that the predominate method that CO2 will be stored underground, isn’t as effective as first thought. The study showed that CO2 coming into contact with brine deposits in underground rock formations — important for the solidification process into solid carbonates — actually causes the CO2 to solidify on first contact, creating a barrier to further CO2 disposition.

Then there is the energy penalty of CCS, which could be as high as 40%, a decrease in the efficiency of a power plant utilising CCS, effectively defeating the purpose of implementing CCS in the first place. The conclusion is that CCS will be limited in its effectiveness to reduce CO2 emissions.

The Committee on Climate Change

A report by The Committee on Climate Change (CCC), Net Zero — The UK’s contribution to stopping global warming, outlines the framework of advice being followed by the Government. It goes without saying that any ambitious process tackling climate change must be global in nature and this is highlighted in the report. It also notes that there are areas where there has been little progress in dealing with the problem. But although many of the recommendations in the report reflect the science, there does appear to be an expectation that technology can offer a silver bullet that will enable the crisis to be solved.

Of the issues already critiqued above, there are other issues mentioned within the report. These are: hydrogen use as a fossil fuel substitute; offsetting; carbon trading and biomass use.

A paper from the Proceedings of the IEEE, highlights shortcomings of using hydrogen as a fuel. Does a Hydrogen Economy Make Sense? poses a question that, according to author Ulf Bossel, is a resounding no. The key point is that:

the energy problem cannot be solved in a sustainable way by introducing hydrogen as an energy carrier. Instead, energy from renewable sources and high energy efficiency between source and service will become the key points of a sustainable solution.

Bossel presents clear analogies using figures that demonstrates the differences in energy efficiency between hydrogen fuel and direct electrical use. The infrastructure involved in mass producing hydrogen would be immense, with a network of power plants purpose built for producing hydrogen. High energy input is required to produce hydrogen. Then there is the stages in between, involving cooling, storage, transport and finding space to store at point of use. All these stages require high energy use. The following infographic shows the energy loses incurred between a vehicle using hydrogen fuel cells and a electric vehicle powered directly from the grid.

To conclude:

Fundamental laws of physics expose the weakness of a hydrogen economy. Hydrogen, the artificial energy carrier, can never compete with its own energy source, electricity, in a sustainable future.

Bossel's argument is scientifically sound. However considering the bigger picture and potential problems surrounding renewable energy storage, hydrogen may have a role to play in a wider energy mix.

Carbon trading and offsetting

Carbon trading and offsetting were introduced as an economic solution to curbing emissions. But trading on carbon markets isn’t going to suddenly cut the amount of GHG in the atmosphere. The EU Emissions Trading Scheme (EU-ETS) has been a central plank in carbon trading. However it has proven unsuccessful in application, as Friends of the Earth Europe outlines in the report, The EU Emissions Trading System: failing to deliver. The EU-ETS is a cap and trade system. A cap is agreed on GHG emissions. Whatever is emitted beyond the cap is traded on the market as tradable permits. The cap consists of allowances that are allocated to companies allowing them to emit a certain amount. Excess allowances can be ‘banked’ for future use.

An underlying problem with the EU-ETS has been over allocation. As FoEE points out in the report:

Greenhouse gas emissions increased in the first EU-ETS phase (2005–2007), clear evidence that the cap was too high and that there was a massive overabundance of emissions. Yet little has been done to close the loopholes. Instead, the Emissions Trading System is acting as a money-making machine for Europe’s biggest companies.

One of the effects of this is that consumers are picking up the tab:

Not only are businesses not reducing their emissions (thanks to excess permits) but they are making extra profits out of the EU-ETS by passing on the costs to consumers. In effect, consumers are paying twice: once for the costs of setting up the carbon market, and once again through higher energy bills.

As a result of these anomalies within the EU-ETS, polluters have engaged in offsetting as a way round the problem. Offsetting is incorporated into the United Nation’s Clean Development Mechanism (CDM). This is defined in Article 12 of the Kyoto Protocol, which allows countries to implement an emission-reduction project in developing countries. This assumes of course that whatever is being offsetted against is actually delivering genuine GHG reduction results. As the report points out, there are shortcomings within this system also. This is an issue that the CCC report recognises:

Most sectors will need to reduce emissions close to zero without offsetting.

Biomass

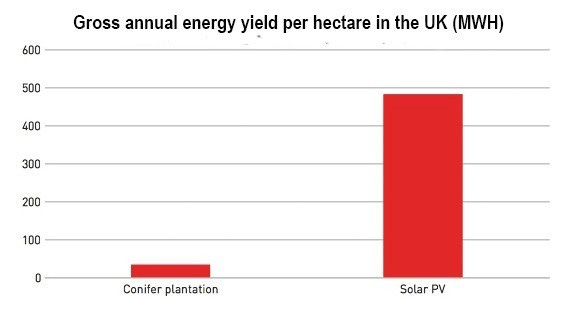

Biomass use has already been touched on above. The report recognises that utilising biomass on a large scale isn’t possible and recommends cultivating biomass carbon sinks wherever possible. This is an issue that has been under scrutiny by campaign Group Biofuelwatch. They point out that, in addition to the points noted above, using biomass as a fuel source is highly inefficient. Taking account of carbon production through photosynthesis, the following graph compares energy yield from a biomass source compared with Solar PV:

Using biofuels is no substitute for fossil fuels. It generates the same problems.

Business as Usual

Rather bizarrely, at the time of writing — exactly 2 weeks after the zero emissions announcement — the UK Government then announced a new round of offshore licensing. The Oil and Gas Authority (OGA) launched the 32nd Offshore Licensing Round. This would open up ‘768 blocks or part-blocks on offer across the main producing areas of the UK Continental Shelf (UKCS). Acreage is on offer in the Central North Sea, Northern North Sea, Southern North Sea and the West of Shetlands.’

Much of the announcement boasts about ‘groundbreaking data packs’, which are ‘carefully targeted’ and ‘ value-adding’. Dr Jo Bagguley, Principal Regional Geologist at the OGA is ‘particularly excited about the geochemical database and the release of the SNS Megasurvey’.

The rest of us are particularly alarmed about this development. And with good cause. There can be little doubt that the Government would have been aware of this forthcoming announcement when it parroted what has now effectively become a zero emissions charade.

Time For Change

In May 2019, a collaborative report by Oil Change International, Friends of the Earth Scotland and Platform London, Sea Change: Climate Emergency, Jobs and Managing the Phase-Out of UK Oil and Gas Extraction, was released.

The proposed expansion of offshore exploration comes in the wake of a steady decline in North sea oil and gas production, leading to job cuts in the industry. The proposal also runs alongside the UK Governments continued support for onshore oil and gas extraction through unconventional means such as fracking. The following graph shows how offshore production has peaked and declined since the industry first opened up in the late ‘60’s:

The report discusses carbon budgets and how they relate to the limits prescribed by the Intergovernmental Panel on Climate Change (IPCC) relative to the outcomes of the Paris agreement. To limit global temperature rise to 1.5°C as stipulated in the Paris agreement, there is a limit to the level of GHG emissions. To meet these emission standards, up to 75% of known fossil fuel reserves need to be left in the ground.

Under a business as usual scenario, there is a danger of ‘carbon lock-in’. If more infrastructure is built around fossil fuel extraction ‘it will be more politically and economically difficult to leave these reserves unextracted compared to reserves that have not yet been developed.’ This could lead to stranded assets in a situation where the entire industry undergoes a sustained collapse. As such the report outlines two possible scenarios whereby we have a ‘deferred collapse’ leading to a rapid decline following a business-as-usual trajectory. The alternative is a ‘Managed transition’. This means no more new licensing of future projects and engaging in a phasing out process for current projects. A key element in this process is a ‘just Transition for workers and communities.’ This is the gradual process of moving oil and gas sector jobs into the renewables industry.

There’s an important revelation that is highlighted in this report that pins down just how shortsighted the UK and Scottish Governments approach is towards oil and gas extraction. Even though the licensing round announced is predominately off the Scottish coast, it comes under the jurisdiction of Westminster. But the Scottish Government endorses continued exploration in the North Sea under a hypothetical independent Scotland scenario.

The report outlines that revenue from oil and gas extraction is very small at 0.16% relative to high production countries. This represent a tiny portion of total GDP. The workforce represents 0.3% of total UK workforce. This would make a transition away from fossil fuels relatively straight forward in comparison with countries with lower GDP ratios. It also begs the question as to whether sustained investment makes sense with such low returns on overall investment, whereas in countries with high production ratios, oil revenue forms a high proportion of economic output, as the following infographic from the report shows:

It would appear that the answer to the question is tied to a distorted perception in the use of fossil fuels. As the report notes:

[T]he government considers climate change and energy more narrowly, only in relation to the combustion of fossil fuels, not their extraction.

Whilst the UK Government has waxed lyrical about cuts in coal extraction, what’s become clear is that there is every intention to replace coal with increased oil and gas extraction. The coal cutbacks generated a 38% fall in UK CO2 emissions. The report calculates that CO2 emissions from oil and gas production could triple, based on current production figures and projected emissions from future developments. This would cancel out the gains from phasing out coal.

In Scotland, a 42% reduction in emissions was reached in 2016, thanks to the complete phasing out of coal. But what’s really interesting here is what would happen if Scotland gained independence. If an independent Scotland pursued full scale offshore development, the main proportion of oil and gas production would be incorporated within the Scottish economy. This might offer a temporary boost, but it would turn the country into one of the worst climate villains on the planet. A remarkable irony given that the 2009 Scottish Climate Change Act was the most progressive at the time. As the report says:

The UK and Scottish Governments’ primary objective for offshore oil and gas is to enable as much as possible to be extracted.

If this strategy was to be followed on the global scale, we would end up with catastrophic climate collapse. The only responsible move from the UK Government would be to reverse the new offshore licensing round. The Scottish Government also needs to get its house in order. There is huge renewables potential in the country that is being neglected. In addition the industry is unsustainable financially. The report exposes an industry that is being run more like a lottery. In short, the industry gets more from the UK Government in handouts than it gives in taxes. Thanks to these handouts, oil and gas fields that would have been otherwise unviable are being developed in what could be described as ‘zombie’ fields.

Tellingly the UK has been deliberately opaque about the use of subsidies:

A comparative survey of G7 countries led by the Overseas Development Institute found that the UK’s transparency was “extremely poor”, that it had failed to publish specific reports on fiscal support to fossil fuels and that it had not participated in a G20 peer review process.

The report outlines three main subsidies:

Tax allowances: This is tax exemptions to ‘ease the pain’ of setting up new infrastructure and subsequent exploration, especially now that easily accessible production is gone and new exploration is more challenging. The aim is to increase extraction come-what-may, generating what the report describes as ‘zombie energy’. This creates additional fossil fuel lock-in effects.

Reduced Tax Rates: This directly impacts tax revenue for the Government. The UK has the lowest tax rate amongst other producers:

[T]he UK effective tax rate since 1990 has averaged 18%, compared to 31% for Germany, 33% for Denmark, 46% for Norway and 48% for the Netherlands. Whereas in 2017 the UK Government received just US $1.86 from each barrel of oil, its North Sea neighbours received respectively $10.35, $8.45, $13.53 and $10.78.

Decommissioning:

Almost half of the costs of decommissioning are set to be covered by the taxpayer.

That’s a sobering thought as we project into a future where the sun sets on North Sea oil and gas production. This is a fairly unique situation compared to other industrial operations, whereby favouritism is apparently extended to the oil industry.

There is a lot of uncertainly related to future decommissioning costs. So its unknown what the final taxpayer bill may eventually be. Estimates range from £58 billion to £100 billion.

To add insult to injury, the Government back in 2013 set up a bizarre legislative process that would make it almost impossible for future Governments to change the rules. It gave companies:

a legal guarantee that future elected governments could not change the tax rules on decommissioning. The new Decommissioning Relief Deeds specified that if a future elected government were to change the tax rules — conventionally always seen as a sovereign matter — it would have to compensate the companies from the public purse.

A familiar Government mantra is jobs, jobs and even more jobs. But what this report clearly points out is that jobs are expendable. Jobs in the industry have steadily declined. Even during periods when the oil price was high. Its all about the bottom line regardless.

The report sets out a plan in which a Just Transition of industry and jobs over to a renewables based economy can take place. It makes sense with the cost of renewables dropping and with energy costs across the board set to drop.

There are two choices. Either the transition can be planned or the oil and gas industry will find itself displaced through natural selection. There is a high likelihood that climate change will force the issue at some point.

Meanwhile the contradictions continue as the UK Government announces plans to install electric car charge points in every new-build home in England.

What has become clear here is that whatever public announcement is being made on climate change by Government, it’s the opposite of the actual intent. Plain logic dictates that you cannot achieve net zero emissions and maximise oil and gas extraction at the same time. Therefore the answer to the question posed by this article is pretty obvious.