The Global Corporate Banking Scam

With COP27 coming to an ignominious close and more attention focused on the banks, this piece outlines how the financial sector is holding the world to ransom.

Another year and another episode of that long running soap opera, which stages the plight of a UN institution tackling the climate crisis, under pressure from con-men and all sorts of baddies. We must hold our breath as the next installment beckons next year as COP28 keeps the drama going ad infinitum.

One of those ‘baddies’ is the banks. They are the arteries of the system. They pump the fiscal life blood and keep the beating heart of the system going, pumping billions into the global energy system and everything else. This report discusses the relationship of the banks with the energy system.

The Fossil Fuel Swindle

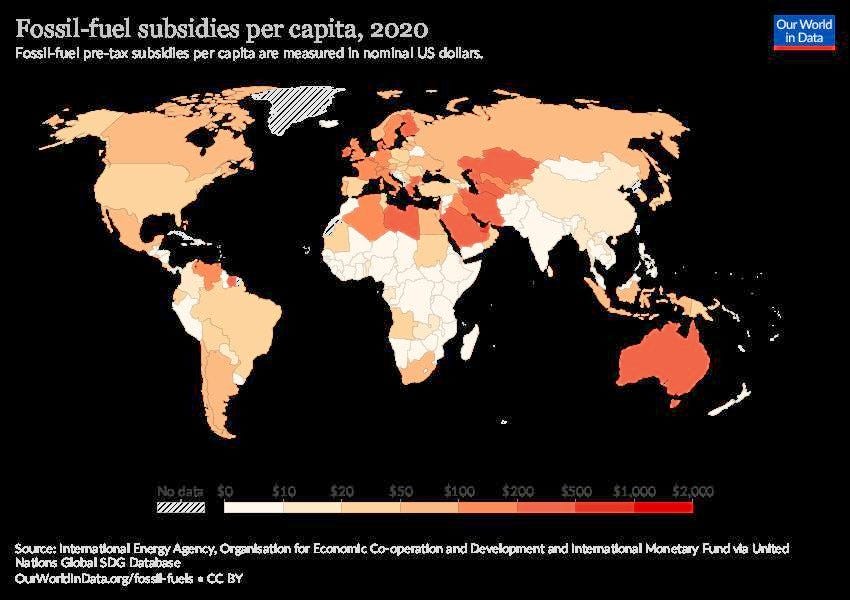

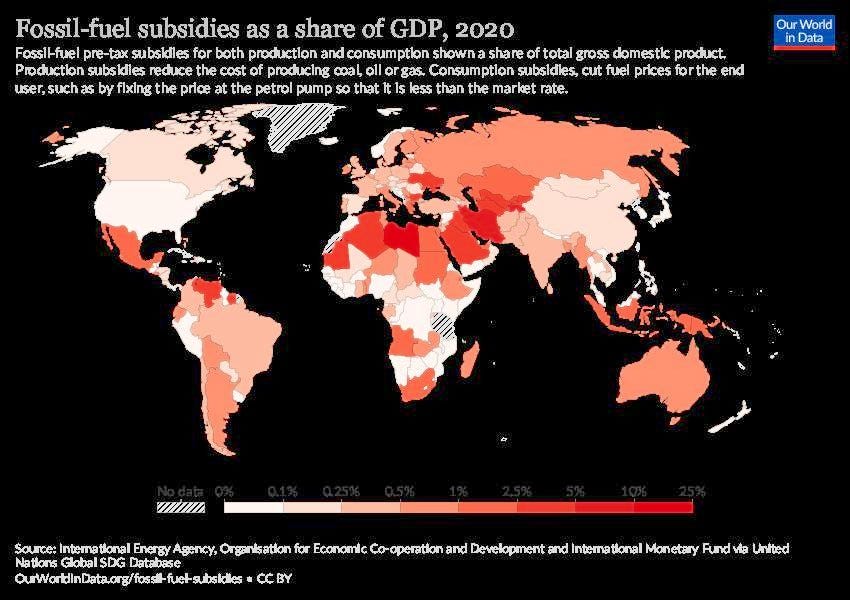

Since 2007, the International Energy Agency (IEA) has been recording fossil fuel subsidy data. According to the Agency, global subsidies rebounded in 2021, following a fall during the pandemic, to $440 billion. How does this break down? Our World In Data has produced maps showing the level of subsidies across the world in terms of per capita and share of GDP:

As the article notes, these are explicit subsidies. Another article covers implicit subsidies. It states:

One way to think about the distinction between explicit and implicit subsidies is that for the former the government has to pay costs from the available budget, in the latter the prices are suppressed, it is the lack of charging that is the cost.

In short, an explicit subsidy is a direct subsidy to bring down the cost of production, whereas the latter fails to cover the costs of externalities caused by fossil fuel use.

According to the IMF, subsidies are inefficient and uneconomic. It notes that:

Globally, fossil fuel subsidies are were $5.9 trillion or 6.8 percent of GDP in 2020 and are expected to increase to 7.4 percent of GDP in 2025 as the share of fuel consumption in emerging markets (where price gaps are generally larger) continues to climb. Just 8 percent of the 2020 subsidy reflects undercharging for supply costs (explicit subsidies) and 92 percent for undercharging for environmental costs and foregone consumption taxes (implicit subsidies).

It may seem surprising that the IMF is calling for a reform on subsidies. This goes back to 2009, when the G20 group of Countries pushed for the phase out of fossil fuel subsidies. At COP26, ‘197 countries agreed to accelerate efforts to phase-out inefficient fossil fuel subsidies.’ But this hasn’t materialised.

Our World argues that a carbon price should be introduced across the board. This would ensure that those causing emissions would actually pay for them. One way to do this is through ‘cap and trade’, another is a carbon tax. Thus:

In a ‘cap and trade’ system the carbon price changes over time. A maximum level of pollution (a ‘cap’) is defined and manufacturers need licenses to emit carbon. How expensive these licenses are is determined by a trading system. The price of a license increases as emissions approach the cap.

A carbon tax is simply a levy that is applied to all goods and services which lead to carbon emissions in their production.

This can lead to fairer subsidies whereby poorer people can get compensation to cover the additional costs incurred by these measures. The idea is that high consumers will end up paying more for their carbon intensive lifestyles.

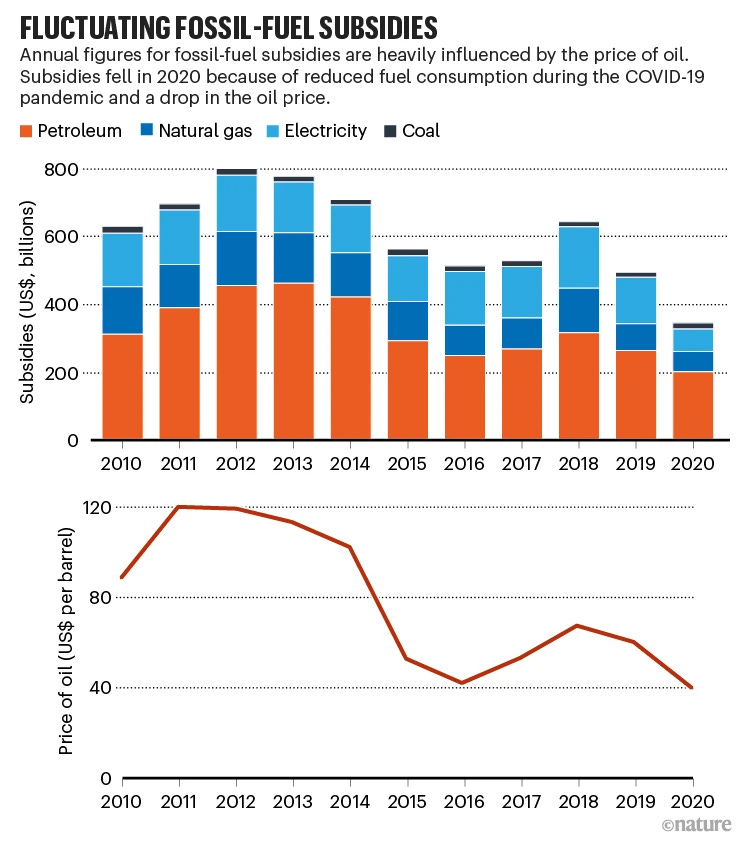

But progress is slow. An article from Nature explains, Why fossil fuel subsidies are so hard to kill. It’s a major obstacle towards the transition to sustainability. In the west, fossil fuel companies’ bottom line benefits from subsidies. The following infographic shows how subsidies fluctuate with prices.

Part of the problem is defining context. When is a subsidy a subsidy? And what exactly is ‘inefficient fossil fuel subsidies?’ Three barriers are cited against removing subsidies:

First, fossil-fuel companies are powerful political groups. Second, there are legitimate concerns about job losses in communities that have few alternative employment options. And third, people often worry that rising energy prices might depress economic growth or trigger inflation.

But these shouldn’t get in the way. The money saved can be used to offset rising energy prices, something that’s being done to tackle the cost of living crisis in 2022, but this is not coming from reduced subsidies. Low oil prices can create the conditions for removing subsidies as prices can rise to compensate within acceptable levels, provided low income families can benefit from cost relief.

From a climate change perspective, the article notes that:

Removing consumption subsidies in 32 countries would cut their greenhouse-gas emissions by an average of 6% by 2025, according to an IISD July report. This chimes with a 2018* United Nations report suggesting that phasing out fossil-fuel support could reduce global emissions by between 1% and 11% from 2020 to 2030, with the largest effect occurring in the Middle East and North Africa (see ‘Carbon cuts’). That reduction could be amplified if the money that would have subsidized fossil fuels was instead used to support renewable energy.

(* link is for 2021 report).

And there is a major disparity, whereby 70% of subsidies went to fossil fuels and ‘only 20% went to renewable power generation.’ Crucially the article warns of diverting subsidies to new fuels such as blue hydrogen and CCS.

Apparently, the UK doesn’t do subsidies! Ethical Consumer though came to a different conclusion. It is noted that:

the UK’s tax regime makes it the most profitable country in the world to develop big offshore oil and gas projects. Most spending on oil and gas exploration can be offset against tax, as it is classified as ‘research and development’. Almost all spending on new fields can be offset in the first year of development, and companies can claim tax relief for decommissioning offshore installations.

Since the Paris Agreement, the government has provided £13.6 billion in subsidies to the UK oil and gas industry. From 2016 to 2020 companies received £9.9 billion in tax relief for new exploration and production, including £15 million of direct grants for exploration, and £3.7 billion in payments towards decommissioning costs.

Ironically following a recent court case, the UK Government was forced to admit that oil and gas companies make more from subsidies than they pay in tax. With extensive lobbying on this front, the oil giants ‘have paid next to nothing in tax while receiving hundreds of millions in handouts.’ Contrast this with other countries such as Norway, which, ‘receives about $21 per barrel of oil’, whereas the UK ‘receives less than $2.’

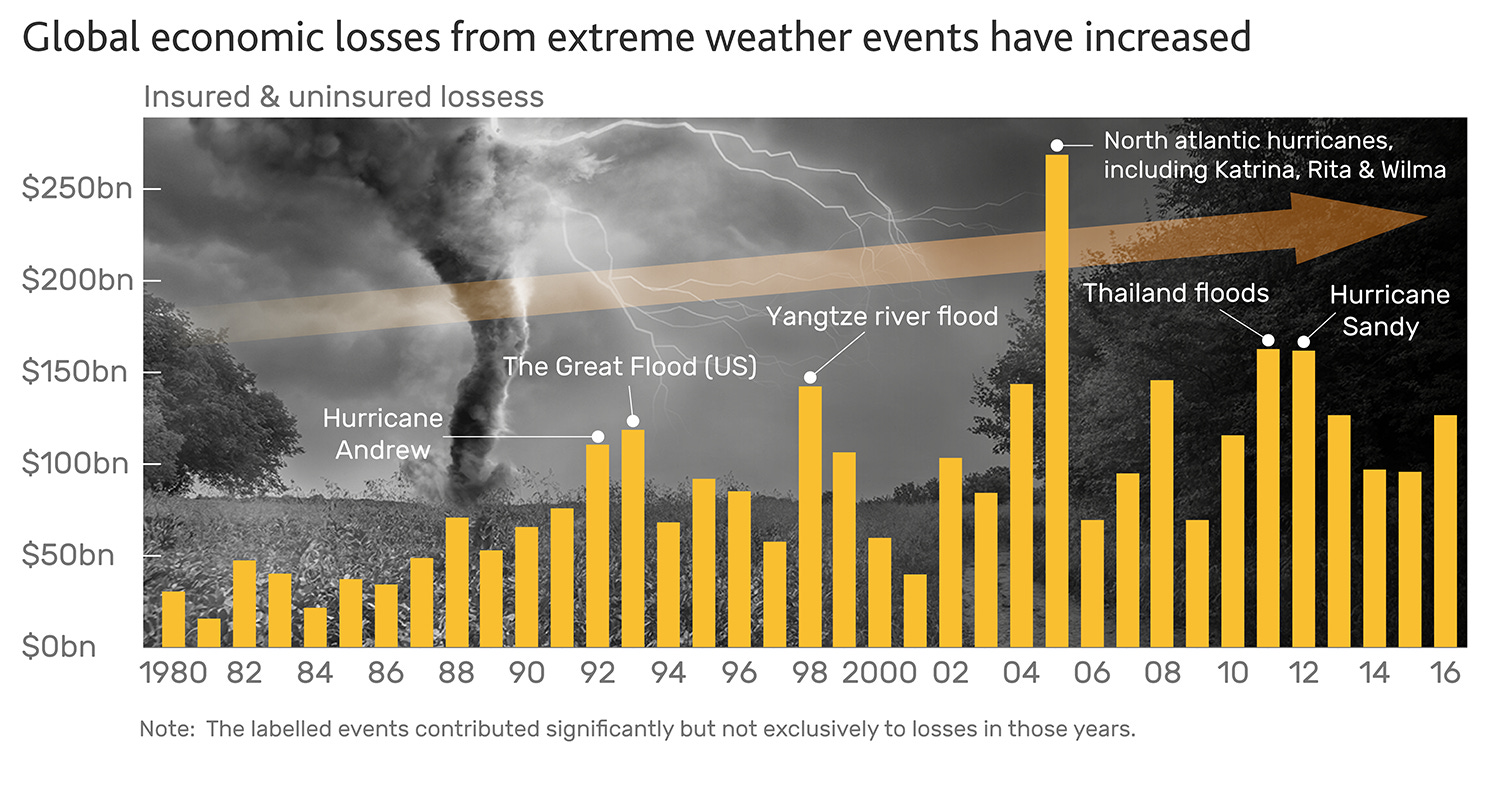

Meanwhile the Bank of England has been reporting on fossil fuel investments and financial stability. This follows an earlier detailed report. It highlights the physical impacts of extreme weather events and how the economy could be affected from increased insurance claims. In short, global economic losses have increased as this graph illustrates.

The article highlights the need to consider the transition to a greener economy and how this can be effectively managed. So what about the role of the wider banking sector? The World Bank is making reassuring noises, as this article from the bank outlines. In 2013, the World Bank introduced the Energy Sector Management Assistance Program’s (ESMAP) via the Energy Subsidy Reform Facility (ESRF). This is supposed to provide a framework to enable Governments to shift away from subsidies whilst safeguarding any impacts on poor people. However as we’ll see later, the World Bank doesn’t exactly have a great track record. But lets move on to the big banks and the role they play in Fossil fuel financing.

Historically 3 top UK banks financing fossil fuel’s were the Royal Bank of Scotland (RBS), Barclays and HSBC. The case of RBS is worth delving into. After the bank was bailed out following the financial crash, it moved about 25% of the bailout money (£45.5 billion) into the fossil fuel sector, most of it into tar sands investments in Canada and Madagascar. They financed Cairn Energy to the tune of £116 million towards their controversial offshore drilling operations near Greenland.

RBS also awarded corporate loans during the US coal rush from 2004 to 2005. This money was put towards mountaintop removal coal mining, responsible for severe water pollution in some of America’s poorest regions in the Appalachian mountains, through waste water from cleaning coal and the dumping of waste earth in or near streams.

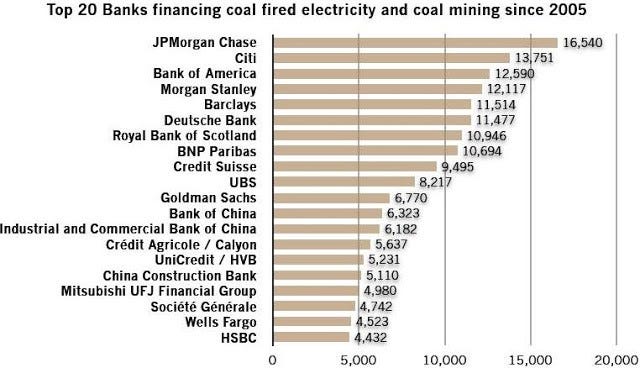

A comprehensive report from BankTrack from 2011, Bankrolling Climate Change, gave a detailed insight into the extent of major world banks’ investments in fossil fuel projects, with a focus on coal.

Coal is certainly the largest contributor to Greenhouse gas emissions. Ending emissions from coal “is 80% of the solution to the global warming crisis,” according to former NASA climate scientist James Hansen.

The report points out that:

Coal-fired power plants are not cheap to build. Typically, a 600 Megawatt plant will cost around US$ 2 billion. Power producers therefore rely heavily on banks to provide and mobilize the necessary capital for such ventures. As much of this financing is indirect — delivered through corporate loans and bonds — banks have for the most part been successful in keeping these investments hidden from public scrutiny.

In 2010, financing for the coal industry was almost twice as high as in 2005 — despite the financial crisis. The research has revealed that since 2005 (the year the Kyoto Protocol was ratified) the total value of coal financing provided by the banks amounted to 232 billion Euros.

Below is a league table which details the investments made by the top 20 lenders. These alone amount to over 171 billion Euros — almost 75% of the total lending (figures in million Euros):

Clearly the biggest culprit investing in fossil fuels overall is US giant JP Morgan Chase. Indeed the investment bank has been implicated in contributing to the financial crisis, particularly with respect to the collapse of Lehman Brothers, which triggered the crisis.

The environmental impacts of coal

I’ll give a brief synopsis here of the impacts coal has on the environment and the people involved in the industry. The Bankrolling report states that:

The entire process from mining through combustion to waste disposal has a dire impact on the environment, human health and the social fabric of communities living near mines, power plants and waste areas. It severely disrupts ecosystems and contaminates water supplies. It emits other greenhouse gases like nitrogen oxide and methane as well as toxic chemicals such as mercury and arsenic. It displaces communities and destroys livelihoods. Of course, none of these costs are reflected in the price of coal. These costs are paid by society — and the heaviest price is often paid by the poor.

Open cast mining can devastate huge tracks of land generating dust plumes, whilst underground mining can cause subsidence over large areas. It notes the impacts of mountain top removal:

After mountains are leveled, the leftover dirt and rock — full of toxins from the mining process — is dumped in local valleys. In the United States alone, over 2,000 miles of streams have been buried or polluted by mountaintop removal. Heavy metals like cadmium, selenium and arsenic poison the local water supply. Mountaintop removal also pollutes the air with hazardous particles. Recent studies have found that cancer rates are twice as high for people who live near mountaintop removal sites.

It’s estimated that coal mining could be responsible for about 25% of methane emissions, not to mention that coal generates more CO2 unit for unit than other fossil fuels. Burning coal in coal fired power plants:

requires huge amounts of water for cooling purposes and they produce huge amounts of waste. Known as coal combustion wastes, these toxic by products are both solid and liquid. They include fly ash from the smokestacks and bottom ash (from the bottom of the boiler). They also include the particles and chemicals trapped by pollution controls like scrubber sludge. Finally, they include many low volume wastes like run-off from coal reserve piles and liquid wastes from cleaning operations. Although some solid coal wastes are used in construction materials, most coal wastes are either destined for landfills or surface impoundments.

In the past acid rain and smog were huge problems. These issues have by and large been dealt with. But in emerging economies such as China and India, that saw rapid expansion of the coal industry, these problems have returned.

Campaigning by civil society groups has been intensifying and it has become increasingly targeted towards the banks. The main message banks should be getting is that their reputations are on the line and that this process will intensify. What they need to acknowledge is that their biggest impact on climate is, in fact, through their core financial business. And there does seem to be a gradual realisation that there has to be a shift from ‘business as usual’.

The first step in this process was the adoption of the Equator Principles, established in 2003 by the banks, ‘in order to ensure that the projects we finance are developed in a manner that is socially responsible and reflect sound environmental management practices’. And ‘negative impacts on project-affected ecosystems and communities should be avoided where possible’. These were followed by the carbon and climate principles.

Officially:

The Equator Principles (EPs) is a credit risk management framework for determining, assessing and managing environmental and social risk in Project Finance transactions. Project Finance is often used to fund the development and construction of major infrastructure and industrial projects.

These are of course voluntary guidelines, but they have been adopted by many of the worlds financial institutions. The EPs have become the industry standard for environmental and social risk management and financial institutions, clients/project sponsors, other financial institutions, and even some industry bodies refer to the EPs as good practice.

Currently 77 adopting financial institutions (75 EPFIs and 2 Associates) in 29 countries have officially adopted the EPs, covering over 70 percent of international Project Finance debt in emerging markets:

The EPs were launched in Washington D.C. on 4 June 2003 and were initially adopted by ten global financial institutions: ABN AMRO Bank, N.V., Barclays plc, Citi, Crédit Lyonnais, Credit Suisse First Boston, HVB Group, Rabobank Group, The Royal Bank of Scotland, WestLB AG, and Westpac Banking Corporation. Subsequently there were over forty further EP adoptions during the first three year implementation period.

The EPs only apply to projects of US$10 million and above.

There are 9 principles which any project should conform to. Briefly these are:

Review and Categorisation

Social and Environmental Assessment

Applicable Social and Environmental Standards

Action Plan and Management System

Consultation and Disclosure

Grievance Mechanism

Independent Review

Covenants

Independent Monitoring and Reporting

The framework of the EPs incorporates the International Finance Corporation’s (IFC) Performance Standards on Environmental and Social Sustainability, part of the IFC’s Sustainability Framework.

This poses a question. The IFC is the private sector arm of the World Bank. The World Bank has a rather dubious history. So, is the EPs nothing more than a highly elaborate greenwash scheme that financial institutions can incorporate into their corporate responsibility structures in order to create a good impression? Certainly the World Bank is trying to improve its environmental image. Was the IFCs Sustainability Framework an effort to consolidate this image?

A Friends of the Earth International (FoEI) report, World Bank: catalysing catastrophic climate change (2011), examines the Banks investment in high carbon infrastructure and the knock-on effects of its policies in developing countries.

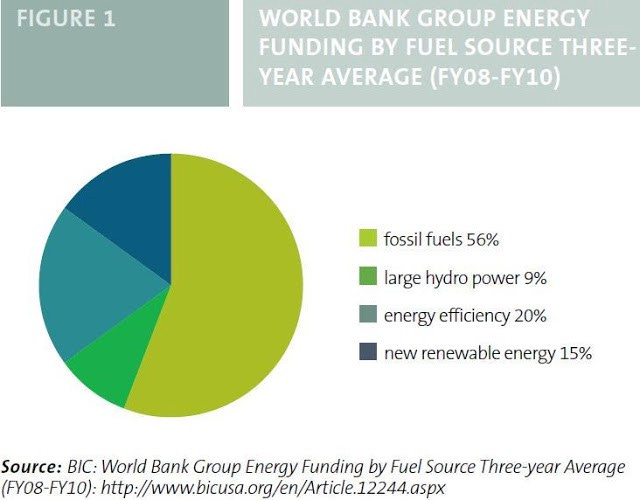

Overall the World Banks’ contribution to GHG emissions is estimated to be around 7%. Much of the investments made by the World Bank — via the IFC — were targeted towards coal based projects, mainly in developing and emerging economies, such as India, locking these economies in to fossil fuel dependence when they could be better served by a solar power based infrastructure. The following chart shows the distribution of World Bank investments:

The Bank tends to emphasize the social and economic benefits of large scale investment, but as several case studies within the FoEI report illustrate, this is generally not the case.

Another major area of investment for the World Bank is large scale hydropower schemes. The whole argument that huge dams can be a safe source of renewable energy doesn’t hold water:

The World Bank has been increasing investment in large hydropower since 2003, following a lull in such investment in the 1990s, and wrongly sees large hydropower as a solution to providing large-scale electricity in a climate-constrained world.

As a source of energy, hydropower is far from being as clean as the Bank claims: it causes devastating social and environmental impacts around the world, and has already displaced 40–80 million people, impoverishing most of them in the process… Dams are also a source of greenhouse gases, especially in the tropics. Scientific studies have shown that decomposing organic matter in reservoirs caused by dams has resulted in significant emissions of the greenhouse gases methane, nitrous oxide and carbon dioxide.

Has anything changed over the last decade? Not really, as this article from Climate Home News reports. David Malpass, the Donald Trump appointed president of the bank, was unable to make up his mind on the scientific consensus on global warming, finally blurting out, “I’m not a scientist”.

Calls have been made for a change of leadership at the Bank. Proposals for reform have been put forward. But such is the current state of affairs that:

Analysis by The Big Shift, a coalition of NGOs, found that the World Bank provided more than $14 billion in financing for fossil fuels since the Paris Agreement was adopted. While it has committed to end financing coal as well as oil and gas extraction, its subsidiaries are still backing fossil fuel projects.

The Banks’ claims to tackle poverty and climate change ring hollow as the combined effects of climate change, the pandemic and the war in Ukraine are plunging many countries, particularly developing countries, into high levels of debt.

Carbon markets

After the Kyoto Protocol came into force, the World Bank set up its Carbon Finance Unit to promote an expanding carbon market. Through this it has been funding carbon trading schemes. As the FOEI report notes, carbon markets have been heavily criticised because they:

have failed to reduce emissions, are inefficient, volatile and susceptible to fraud. Indeed, factors such as these are fueling the rate of growth because of an increased volume of speculative trading, and take up by those intent on engaging in value-added tax (VAT) fraud in the EU Emissions Trading Scheme, as well as the sale of surplus pollution permits cashed in by EU companies during the economic recession (Reyes, 2010). Of the US$144 billion carbon market, only US$3,370 million goes to project developers (and only a fraction of that will go to communities who host projects).

The Bank also provides funding for projects that come under the Clean Development Mechanism (CDM). But this system has been abused and has been poorly regulated by the bank. An example has been large hydro schemes, as noted above.

The World Bank has also got involved in the Reducing Emissions from Deforestation and Degradation (REDD) scheme. Again this has come under criticism as no formal structure has been agreed. However projects have been rolled out incorporating REDD, which have done more to exasperate the problem of deforestation. As REDD-Monitor points out, ‘REDD has failed.’ It notes that:

Ellysar Baroudy, the coordinator of the World Bank’s Forest Carbon Partnership Facility, recently inadvertently acknowledged as much. In an interview marking 10 years of the FCPF, she said that,

“We’re all aware that deforestation rates continue to rise. And they’re rising for various reasons. They’re rising because agriculture is needed, and so people are cutting down trees to make space. It’s rising because people need energy, so they’re cutting wood for fuelwood.”

Baroudy focusses on people as the drivers of deforestation. She could have pointed out that corporations are clearing forests to make way for oil palm plantations. She could have described the destruction caused by corporations involved in industrial logging. Or industrial tree plantations. Or soya plantations. Or cattle ranching. But she doesn’t. People, then, are the problem, according to Baroudy.

Another major area of controversy has been the adoption of the World Bank as trustee for the Green Climate Fund (GCF). FOEI explains the background to the fund. As part of the Framework Convention on Climate Change (UNFCCC), the fund does not finance directly, it does so via an intermediary. The World Bank Group was accredited in 2015. The GCF lists its Accredited Entities here. Despite initially being setup in the Cancun talks in 2010, it was slow to emerge. As Nature reports, it has been bogged down by lack of transparency and funding. Part of this is linked to available cash flowing through the likes of the World Bank rather than directly funding projects. The GCF is also poorly run and has low confidence within staff. Add to that the failure of the US to honour its commitments to the fund, its future may be short-lived.

This brings us back to the validity of the EPs and the question over the World Banks’ green image. The FoEI report sums up with this conclusion:

the World Bank — with its troubling record on the environment, human rights, climate impacts, and development — needs to be exposed and held to account for its role as a major climate polluter with an appalling sustainable development track record.

The harmful solutions that are promoted by the World Bank, including carbon market-based mechanisms such as REDD, industrial monoculture tree plantations, agrofuels, so-called “cleaner” fossil fuels and large dams aim to increase the profits of investors by further privatising and commodifying nature.

The Bretton Woods Project — an organisation set up to monitor and scrutinize the World Bank — has also been critical of the IFC. In the article Out of sight, out of mind?, how IFC investments are funneled through the banking sector are examined.

Instead of financing projects directly, the IFC has a policy of divesting funds through the financial sector. This means that funds could end up in the big banks, who’s social and environmental awareness are effectively zero.

Investments made by the IFC could also end up in tax havens. The main issue highlighted in the article is the total lack of transparency of these processes. There is no strategy in place for tracking what happens to funds once they leave the IFC — quite literally ‘out of sight out of mind’.

So, is the IFCs new Sustainability Framework an effort to address its critics? The Bretton Woods Project has its doubts. In another article it reports that the reforms only partly address some of the concerns made by its critics.

There’s nothing green about the World Bank and it certainly doesn’t eradicate poverty. And the EPs equate to very little. And what about the Carbon Principles and the Climate Principles? The Bankrolling Climate Change report sums it up:

The Carbon Principles, which were adopted by several U.S. banks and Credit Suisse in February 2008, only target the financing of new coal power plants in the United States. Moreover, their focus is reducing risks to the banks through anticipated regulatory responses to climate change rather than limiting the actual climate impacts of banks’ investments. As Rainforest Action Network pointed out in its latest report The Principle Matter — Banks, Climate and the Carbon Principles, published in January 2011, “There is no evidence that the Carbon Principles have stopped, or even slowed financing to carbon-intensive projects.”

The Climate Principles, which were adopted by HSBC, Standard Chartered, Credit Agricole, Swiss Re and F&C Asset Management in December 2008 and joined by BNP Paribas in June 2010, have a broader scope, but nonetheless follow the same trend as the Carbon Principles. They focus on due diligence procedures and managing the economic risks of climate change for banks’ business instead of setting standards that will actually reduce the carbon footprint of banks’ portfolios.

Toxic Investments

In the 2011 report Unburnable Carbon — Are the world’s financial markets carrying a carbon bubble? the Carbon Tracker Initiative set the scene with a report that should have made even veteran investors gulp on their espressos. Since then, CTI has updated the report, issuing Unburnable Carbon: Ten Years On.

The first point to make is that little has changed since the initial report. Some of the predictions and parameters have become more urgent. On the positive side there is an inexorable gradual transition towards sustainable energy production as renewables expand and become cheaper and energy storage becomes more efficient. However with the geopolitical instability linked to the war in Ukraine, there is a surge in fossil fuel energy use. This will continue in the foreseeable future.

The report highlights the preoccupation with Net Zero, stating that ‘90% of global GDP is covered by some level of a “net-zero” commitment’. But of course such commitments are largely meaningless unless they translate into something tangible. Importantly though is the change in the carbon budget, which was estimated at 400GtCO2 (in 2020). It is noted that:

With around 78 Gt released over the past two years, this leaves a budget of around 320GtCO2 at the start of 2022; at current rates of fossil fuel production, this budget will be exhausted by 2030 – two decades ahead of the much-heralded 2050 net zero target.

Keeping the whole process going are the global financial centres:

stock markets, and the industry around them such as the asset owners, assets managers, custodian banks and central securities depositories, are:

a. enabling the production of fossil fuels beyond climate limits

b. exposed to transition risk, and

c. potentially failing to achieve their own ambitions of Paris-alignment

A vital point here is embedded emissions in financial centres around the world. This is the estimated emissions from companies listed on stockmarkets. New York and London are key centres along with other exchanges. Interestingly the London stock exchange has estimated reserves of around 47 GtCO2, which is 10 times that of the UK’s legally binding carbon budget for the next 15 years. This creates problems for the City’s net zero aims. As the report points out:

The London Stock Exchange Group plc (LSEG) announced in February 2021 that it has become the first exchange group to commit to net zero through the ‘Business Ambition for 1.5°’ Science Based Targets initiative, and in doing so has become a member of the United Nations Climate Change ‘Race to Zero’.

It’s unlikely though they’ll be an orgy of mass divestment from the Stock exchange in the immediate future. The report continues (emphasis added):

[The] LSEG has launched a Transition Bond segment and is ‘encouraging’ issuers to report against Task Force for Climate-related Financial Disclosures (TCFD) guidelines through reporting guidance. Disclosing climate-related information along the TCFD guidance is not currently mandatory, although the Financial Conduct Authority (FCA) is tightening the rules and the UK Government intends to introduce climate disclosure rules for larger companies, known as the Sustainability Disclosure Requirements (SDR). These are all steps in the right direction, but are they enough?

The report poses the question as well as giving the answer… . The bottom line is that any company trading stocks attracts financial interest. That’s funding fossil fuel companies. And although there has been fluctuations away from some centres, mainly regarding coal divestment, the problem is that ‘the listing of embedded coal emissions has shifted from the West to the East’ (mainly China and India). The following map shows the distribution of embedded emissions globally.

Following on from this is the risk of stranded assets. This projects equity embedded in future infrastructure and investments under a business-as-usual scenario, expressed as capital expenditure (capex). Such capex could reach a value of $1.9tn. The following table shows the distribution of capex.

Yellow – new projects with some of the lowest breakeven prices, potentially resilient to lower fossil demand under a Paris-aligned (‘well below 2°C’) scenario, but at risk of becoming stranded under faster transition scenarios. We use the IEA’s Sustainable Development Scenario (SDS, 1.65°C), as this Paris-aligned scenario.

Orange – new projects with comparatively higher breakeven prices, which we see as likely to go ahead under a ‘business as usual’ scenario, but at risk of becoming stranded if a Paris-aligned pathway is achieved (SDS). We use the 2.7°C IEA’s Stated Policies Scenario (STEPS), as a proxy for business-as-usual behaviour.

Red – the highest-cost project options that we assess as potentially uneconomic even under a business-as-usual scenario, and if sanctioned then would be highly vulnerable to becoming stranded. Companies developing projects in this band are effectively betting on complete failure of society to achieve global climate goals.

This will impact the major financial centres with New York having significant assets. Moscow also has a large proportion of assets. These will be impacted by the war in Ukraine. As this report was compiled before the Russian invasion, it does not take account of the surge in fracked liquefied natural gas (LNG) being shipped to Europe from the US and the expenditure on gas terminals and other associated infrastructure. I cover this in the Ukraine article.

As the report makes clear, there is little alignment in the industry to the Paris Agreement. It goes on to make a series of recommendations to policymakers and regulators. These are the key points summed up:

The prosperity and wealth created in the wake of the fossil fuelled industrial revolution has hit the buffers of the Earth’s carbon budget

Financial market regulation is not fit for purpose. Price rises in the wake of the Ukraine crisis outline the risks inherent in short term miscalculated fossil fuel investments

Company financial statements should be transparent about climate impacts and embedded emissions

Investment portfolios need to reflect climate risks, taking account of long term fall in demand for fossil fuels.

To conclude:

For those companies who fail to readily align their business plans with a 1.5°C trajectory, even after extensive ‘engagement,’ shareholders always have the option of switching their capital allocation from fossil fuels to alternatives including renewable energy. Divestment should always be a tool in the investor toolbox.

How do the major banks fit onto the equation? Banktrack has produced the report Banking on Climate Chaos 2022. It notes that the French bank La Banque Postale has set a unique precedent to suspend ‘support for all companies expanding oil and gas, and commits the bank to exit oil and gas financing entirely by 2030.’ Unique, because despite 44 of the worlds top banks committing to “net zero emissions by 2050”, the evidence in the short term is business as usual, with planned reductions made through offsetting that simply delays the implementation of essential emissions reductions. Indeed in 2021, those banks earmarked $145.9 billion to the fossil fuel industry.

The legacy speaks for itself, as the report notes:

In the six years since the adoption of the Paris Agreement, the world’s 60 largest private sector banks financed fossil fuels with USD $4.6 trillion.

The following table lists the ‘dirty dozen’ financiers of fossil fuels.

All this comes in the wake of possibly the greatest greenwash in history aka COP26 in Glasgow, which I covered here:

As the report puts it:

The fossil fuel industry is and has been busy greenwashing itself inside and outside the UN climate negotiations, primarily through hyping the need for fossil fuels — even though renewables provide cheaper, safer energy access to communities that lack electricity — and appealing to the public with propositions primarily based on carbon credits and offsets. These appeals often boil down to, “Give us money and we’ll plant a tree to cover your carbon footprint.”

What is perfectly clear is that the fossil fuel industry has made no commitments to ending new expansion. Net zero pledges are basically useless. As the report sums up:

No major oil and gas company has yet released a climate pledge or sustainability plan that meets the bare minimum criteria for alignment with the Paris Agreement, and their bankers need to face this reality when making financing decisions… .

A report from The Transnational Institute (TNI) in collaboration with Corporate Europe Observatory (CEO) outlines how the UN multilateral system of global governance has been captured by financial interests, especially at COP26, in a process defined as multistakeholderism.

The problem outlined in the report is that through the corporate capture of climate summits, ‘the very investors funding greenhouse gas pollution have been put in charge of handling financial markets in the light of climate change.’ At COP26, key fossil fuel investors projected themselves as ‘key leaders in ‘climate finance’’. The Glasgow Financial Alliance for Net Zero (GFANZ) was set up as a front for Big Finance. Put succinctly:

This decision, to go for self-regulation rather than regulation of private finance, leaves the world with a huge problem. There is no solution to the climate crisis without changes to financial markets. If big banks, investment funds, and asset managers can pour endless sums into the development of fossil fuel exploration and infrastructure without restriction and also ‘manage’ the small share that goes to the clean energy sector, we are unlikely to be able to change course away from more disastrous runaway climate change.

The Paris Agreement inadvertently opened the door to Big Finance through the provision of Article 2.1c:

Making finance flows consistent with a pathway towards low greenhouse gas emissions and climate-resilient development.

The emphasis here is on net zero, but should we be talking about real zero?:

It’s worth pointing out here, that ‘net zero’ is an idea – perpetuated by Big Polluters – that their continued emissions can be ‘balanced’ by offsetting, capturing, or removing (from the atmosphere) CO2. Real zero would involve actual emissions cuts starting with a rapid phase-out of fossil fuels and scaling-up of renewable energies. Changing the goalposts from real zero to ‘net zero’ emissions is a sleight-of-hand boon to the fossil fuel industry and its financial investors.

The report quotes a spokesperson from BlackRock:

“In the financial services industry, when people talk about climate risks, they don’t mean risk to the planet; they mean risks to their portfolio…. We’re not trying to stop Miami from getting wrecked by climate change. We’re trying to get our money out before it hits.”

As I outlined in my COP26 article and emphasised here in the report, the build up to COP26 revolved around the firm entrenchment of Big Finance, with tycoon Mike Bloomberg appointed by the UN Secretary General as Special Envoy on Climate Action followed by Mark Carney fitting into the same role acting as finance head. Driven by the United Nations Environment Programme Finance Initiative (UNEP FI), some fancy sounding initiatives were established to give the whole process a veneer of credibility; the Net Zero Asset Managers Initiative, the Net Zero Asset Owners Alliance, the Net Zero Banking Alliance, and the Net Zero Insurance Alliance.

All this was a part of the dynamic sounding Race to Zero coalition. The result was bold statements about how 450 financial institutions had committed to net zero, with an estimated “130 trillion dollars to invest in efforts to tackle climate change”. All this would fall into place by 2050. But in reality it was all just an exercise in Public Relations bullshitting. The $130 trillion:

is the total of investments under administration by the 450 financial corporations in the net zero coalitions. It does not mean they are to be reinvested to support a transition, merely that the institutions that control them have committed to a ‘net zero’ view of a ‘green’ transition.

Although there has been a minor shift in the right direction since COP26, there are nevertheless still discrepancies where net zero by its very nature evades reductions at source in favour of carbon credits, offsets and other dubious false solutions, with a reliance on technical fixes such as carbon capture and storage. Problem is, its all voluntary. There are no regulatory criteria. In short, the ‘Race to Zero’ will eventually be won by a snail. By then it’ll be too late to be effective. The GFANZ has been to go-to club for big finance. Its omnipresence at COP27 was predictable.

What is actually happening then is that civil society is being nudged out of its role as a stakeholder in the UN system. As the report puts it:

multistakeholderism is being presented as the new way of doing it - a way that ignores the long tradition of UN rules and practices and is moving into another formula of inclusiveness that fits better with the idea of ‘key stakeholders, instead of democratic representation and participation.

Clearly civil society needs to respond to this, but so far there has been no collective shift in civil society’s strategic approach.

Food Speculation

It isn’t just fossil fuels and climate change that the banks are up to their necks in. Another issue that has became prominent, is financial speculation, in this case, food speculation.

As indicated above, Barclays bank is the largest financier of fossil fuels in the UK. It has also been the fastest-growing food speculator in the world, driving up food prices. In the second half of 2010 in the wake of the financial crisis, 44 million people worldwide were driven into extreme poverty due to rising food prices.

Global Justice Now published the report The great hunger lottery (2010). They estimated that Barclays made up to £340 million a year from betting, or speculating, on food prices. In the space of five years, the amount of financial speculation on food nearly doubled, from $65 billion to $126 billion.

Extensive evidence has established the role of food commodity derivatives in destabilizing and driving up food prices around the world. This in turn has led to food prices becoming unaffordable for low-income families around the world, particularly in developing countries highly reliant on food imports.

It cites that:

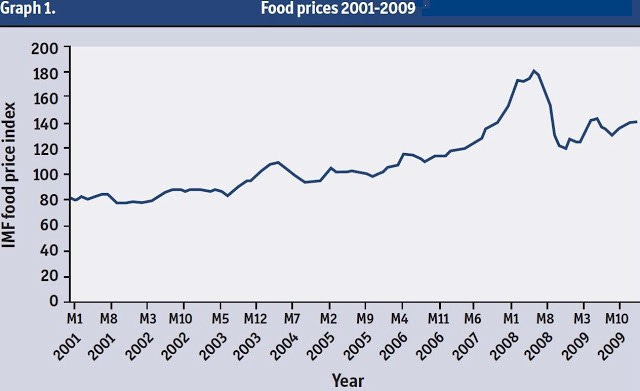

From early 2007 to the middle of 2008 there was a huge spike in food prices. Over the period there was more than an 80 per cent increase in the price of wheat on world markets. The price of maize similarly shot up by almost 90 per cent. Prices then fell rapidly in a matter of weeks in the second half of 2008 (See Graph below). There are various reasons to explain a general increase in food prices over this time. But only financial speculation can explain the extent of the wild swings in the price of food.

The root of the problem — as with many issues — was deregulation. In 1991 persistent lobbying by Goldman Sachs in particular exempted many commodity speculators from the limits on trading created in the 1930s. New and more complicated contracts were created based on the price of food. Derivatives in food, just as in property and shares, expanded massively.

Goldman Sachs then created a Commodity Index Fund, which became the primary vehicle for speculative capital involvement in food commodity markets. The United Nations Conference on Trade and Development (UNCTAD) has stated that:

part of the commodity price boom between 2002 and mid-2008, as well as the subsequent decline in commodity prices, were due to the financialization of commodity markets. Taken together, these findings support the view that financial investors have accelerated and amplified price movements driven by fundamental supply and demand factors.

In other words, food speculators created a bubble:

that lies above everything. Their expectations, their gambling on futures help drive up prices, and their business distorts prices, which is especially true for commodities. It is like hoarding food in the midst of a famine, only to make profits on rising prices.

The rising price of oil during this period was another decisive factor in expanding the bubble, with Goldman Sachs using its position as a financial analyst to push oil markets by making predictions that oil prices would rise. The bank was heavily investing in oil at the time:

An April 2010 survey of banks, traders and oil companies found that 70 per cent say speculation is currently increasing the price of oil [significantly].

A high oil price has many impacts on developing countries. For net oil importers, it increases the import bill. As with high food prices, poor people across the world have to use less energy and/or cut their expenditure on other things. Furthermore, as agriculture is an energy intensive industry, a high and variable oil price has a knock-on impact on food prices’ (Hunger Lottery Report). It goes on to say: ‘Widely changing prices make it difficult for farmers to make decisions about what crops to grow and what to invest precious resources in. For instance, the FAO [Food and Agriculture Organisation] continues: “At the national level, many developing countries are still highly dependent on primary commodities, either in their exports or imports. While sharp price spikes can be a temporary boon to an exporter’s economy, they can also heighten the cost of importing foodstuffs and agricultural inputs. At the same time, large fluctuations in prices can have a destabilizing effect on real exchange rates of countries, putting a severe strain on their economy and hampering their efforts to reduce poverty.

The following table shows the commodity price hikes:

A knock-on effect of the impacts caused by speculation is land grabbing:

Many investors lost money when commodity prices crashed. So some decided to invest in land instead: “Demand for actual physical assets, such as farmland, is very strong among investors in general from high net worth individuals to sovereign wealth funds’, according to Will Shropshire, head of agricultural trading at the London branch of the U.S. investment bank, J.P. Morgan Chase. In other words, agricultural commodities speculation is also a motive for the development of land [grabbing].

So although there were other factors involved in fluctuating commodity prices such as the expansion of biofuels and the effects of climate change, the evidence points squarely at the financial market as the main influence, as this graph from this subsequent report by GJN, Broken Markets, shows. It illustrates the price fluctuation of maize — which was increasingly used for biofuel production — against supply and demand:

Speculation continued to create price volatility well into 2011 — as the graph indicates. This had a damaging impact on food producers. Broken Markets outlined the need for urgent regulation to control what is effectively a commodities casino being driven particularly by investment banks such as Goldman Sachs and Barclays. A report commissioned by GJN details Barclays involvement in these markets.

The effects of price volatility not only impacts producers but has created social unrest, as Broken Markets pointed out:

during the 2007- 2008 food price crisis, food riots took place in 31 countries. In Haiti a week of riots brought down the government and left five people dead, while in Bangladesh 20,000 workers rioted over high foodprices. In 2011 food price rises have been one of the key triggers for the protests in Tunisia, Egypt and Jordan and elsewhere in the Middle East and North Africa, eventually leading to the overthrow of the Tunisian and Egyptian governments.

Economically the effects have been increased cost of food aid to developing countries. One of the main routes that speculators use is ‘over-the-counter’ trading (OTC). This takes place bilaterally and without effective regulatory oversight and prices are not reported publicly, with limited data on what’s going on. This has led OTC trading to be referred to as ‘dark markets’ due to lack of transparency and regulation, which is thought by many to have been at the heart of the 2008 credit crisis, with the G20 resolving to bring more transparency to these markets. As the report notes:

The subprime crisis clearly showed the dangers of unregulated trading in OTC derivatives, yet the risks of this trading in dark markets still exist for agricultural commodities, with potentially even greater risks.

Tracking those OTC transactions is difficult. In the US all futures and options exchanges are required to report traders’ positions daily to the US regulator, the Commodity Futures Trading Commission (CFTC). This detailed position reporting is then aggregated by the CFTC and reported publicly, showing the different positions of different categories of traders. No such reporting to regulators takes place in European markets. Broken markets concludes that:

this lack of rigorous market data is exacerbated by the lack of dedicated regulatory expertise for commodity markets in many European countries such as the UK.

Transparency is vital if excessive speculation is to be controlled with greater cooperation within markets:

Without effective regulation to limit the impact financial speculators can have within the futures market it is likely that prices will become increasingly disconnected from supply and demand fundamentals, become more volatile and continue the dramatic upward trend seen in recent years.

In the UK, the FSA did not exercise its powers to intervene in commodity markets at all in 2010, delegating responsibility to the commodity exchanges and admitting it was not aware how often the exchanges themselves intervened in the markets.

Regulatory expertise and capacity on commodity markets is lacking in the UK and throughout the EU. Dedicated expertise and increased capacity for commodity market regulators is required to ensure any rules proposed are enforced effectively.

The US took steps to introduce regulation. The Dodd-Frank Wall Street Reform and Consumer Protection Act:

Introduces mandatory clearing and exchange trading for commodity swaps, that until now had been traded OTC; Allows for the introduction of individual and aggregate position limits across futures, swaps and options with the stated purpose of tackling excessive speculation.

The EU has developed the Markets in Financial Instruments Directive 2 (MiFID):

Action in Europe is vital to achieving effective regulation internationally. The rules proposed in the US to tackle excessive speculation are at risk as traders threaten to move to less regulated exchanges. By ensuring that clear and strong action is taken in Europe this can prevent the risk of regulatory arbitrage, of competition and deregulation between different trading venues and ensure meaningful regulation of the world’s major food commodity markets.

However in my detailed analysis of the financial system,

I pointed out that:

US banks can circumvent Dodd-Frank by funneling their activities through UK subsidiaries based in the City of London.

Indeed most of the scams committed by huge US financial institutions used the City as a cover up. One bank that is no stranger to scams is Barclays. I detailed the bank’s history of persistent corruption here.

Trade Deals

To wrap up this report, I finish with a note on trade deals, specifically the Energy Charter Treaty (ECT), which I covered in detail in the Ukraine article (above). As I noted:

trade agreements like the ECT act like road blocks when it comes to energy transition. They become suicide packs that stymie action on climate change.

Indeed the ECT played its part in the failure of COP26 and previous summits due to the threat of Governments being sued. But there is hope on the horizon. It would appear that the ECT is crumbling due to a failure in implementing a reform plan at a meeting on the 22 November 2022. As GJN reports, Germany, France, the Netherlands, Spain, Poland, Slovenia and Luxembourg have announced their departure from the treaty, and ‘the European Parliament just voted for exit. The treaty is collapsing.’

If it does collapse, it could open the door to massive divestment from fossil fuels. Indeed it could be the key linchpin that initiates the major reforms necessary to transform the economy and potentially legitimise future UN climate summits. It would certainly make the major banks think twice about where they should invest their money.