Fracking — A Dinosaur Waiting For The Big One

Fracking — A Dinosaur Waiting For The Big One

Natural gas is clean and green - according to the marketing gurus. The war in Ukraine has created a boom for fracked Liquefied Natural Gas (LNG) from the US. But a major collision is on its way...

This article follows on from:

In an apparent contradiction of the persistent trend of banks investing billions in fossil fuels, Mark Carney, Governor of the Bank of England at the time, made an extensive speech in 2015, warning about the impacts of climate change.

The New York Times reflected on Carney’s speech, speaking as he did from Lloyds HQ in London. As the article put it:

Global insurers are already facing a higher frequency of large, expensive disasters from extreme weather, and in the future could face untold liabilities as the losers from a warming planet try to extract compensation from the (insured) companies that profited from fossil fuel production. It was no coincidence that Mr. Carney delivered his speech at the three-century-old insurer Lloyd’s of London.

With tremors from the last financial collapse still being felt, the article offers a stark warning on:

how the effects of a shifting climate could similarly ripple through both the financial system and the real economy in ways that are impossible to predict with any precision today.

The article goes on to say:

Those energy extraction industries, which include many of the planet’s biggest companies, could one day face existential risk. If global governments get more aggressive about restricting carbon emissions, it could mean that billions of investment in oil and gas extraction will be rendered useless and undermine both some of the most widely held investments and the government finances of oil-producing regions.

And as the echoes from Carney’s speech were just beginning to fade, the liability noted above became all too apparent when Peabody Energy, the worlds largest coal company, filled for bankruptcy just over six months later. With its high carbon footprint, coal has been on its way out, with cheap fracked gas filling out the niche and being touted as a low carbon alternative.

A report from the Carbon Tracker Initiative, The US Coal Crash — Evidence for Structural Change, examines the coal crash in the US as a potential harbinger of what’s in store for the fossil fuel industry in general. Coal has been declining for some time, not just in the US but elsewhere. Even China is seeing a decline in coal use as it seeks alternative less polluting energy sources.

The expansion of shale gas production in the US has certainly had a major impact on the coal industry. Regulatory oversight has also increased, extending tighter control over coal production, with an increase in renewables and energy efficiency also having an impact. The report sums up the issue by pointing out that the shift that has taken place ‘has demonstrated that a major developed economy can decouple its economic activity from coal-based power, is a wake-up call.’ But its a call that seems oblivious to the major producers. Given that this report came out before the collapse of Peabody Energy, it makes this interesting and ominous observation:

The largest coal producer in the US, Peabody Energy, appears to treat the signals that have led to such huge financial pain as an aberration, rather than the new normal. In their quarterly report for 2014, Peabody reveals their expectation that in the US, ‘utility coal usage is projected to increase 10 to 30 million tons over 2014 levels’. Furthermore, Peabody expects ‘global coal demand to rise 500 million tonnes by 2017… [with] an estimated 8 to 10% increase in seaborne thermal coal demand’. There are few signs that suggest that either forecast will come close to fruition.

And with regards to the rest of the fossil fuel industry:

Other fossil fuel markets internationally should also acknowledge the extent of stranded assets incurred in the US coal sector. They should use this case study to build their understanding of, and resilience to, the potential value destruction that could result if stakeholders miss the evident trends of ever-falling costs of renewables and improved energy efficiencies driving the transition to a lower carbon energy system.

And this is precisely something that advocates of Unconventional Gas Extraction (UGE) should be taking note of. With firm evidence of underestimated Greenhouse Gas Emissions (GGE), shale gas in particular has now been demonstrated to have a higher carbon footprint than that of coal. That puts the industry at extreme risk. But such risks aren’t just the province of high flying City investors. Many of us have assets in pension funds. This article from the Guardian reveals how the coal crash has impacted pension funds:

The pension funds of millions of local government workers have lost hundreds of millions of pounds in the last 18 months, as the value of the world’s biggest coal mining companies has crashed, according to a new analysis.

The Local Government Pension Scheme (LGPS) provides pensions for 4.6m people, including social workers, school staff, bus drivers, librarians, park attendants and housing officers. The losses estimated by campaign group Platform are equivalent to hundreds of pounds per member.

It also notes:

Another large scheme, the Strathclyde Pension Fund (SPF) lost £26m. “SPF’s main exposure to coal and other fossil fuels is through its listed equity portfolios and the value will vary substantially over time, dependent on the decisions made by active managers,” said an SPF spokesman. “We are a large fund, but our percentage exposure is actually pretty average within our sector.”

Natalie Smith, a lawyer at Client Earth, said pension fund managers could ultimately be sued if they ignored the potential risks of fossil fuel investments. “If pension fund trustees fail to properly manage these risks in their investment decision-making process, and there is a consequential decline in value of the [fund], then trustees and investment managers could be sued for breaching their fiduciary duties.”

And, given the current situation, as the Ferret reports, SPF along with Lothian pension fund in Scotland, ‘have a combined £448m invested in companies which have continued to do business as usual in Russia since its invasion of Ukraine.’ Pension funds elsewhere in the UK have similar investments. On an level playing field, there should be equal concerns towards Russian investments along with other countries who profit from conflict and climate change.

Even prior to the COVID pandemic, the shale gas industry in the US was in a precarious position. During COVID, there was a strong likelihood that this would be the next domino in the fossil fuel chain to collapse. But the war in Ukraine changed all that.

The Platform report referenced above (2015) lists data for UK pension funds. These are the top 5 UK funds:

1. Greater Manchester Pension Fund £1,304 million

2. Strathclyde Pension Fund £752 million

3. West Yorkshire Pension Fund £671 million

4. Merseyside Pension Fund £355 million 5. West Midlands Pension Fund £355 million

The ten authorities with the highest percentage fossil fuel investments are:

London Borough of Merton 10.99% Worcestershire 10.74% Northamptonshire Local Government 10.35% Greater Manchester 9.82% London Borough of Camden 9.5% London Borough of Tower Hamlets 8.76% Teeside 8.74% East Riding Yorkshire 8.73% Dyfed Pension Fund Investments 8.34% Somerset County Council 8.25%.

Based on the figures above, Greater Manchester has the highest proportion of fossil fuels. This would also make it the most vulnerable to fluctuations in fossil fuel investments.

The underlying issue here is keeping investments within the local economy instead of syphoning them off into the coffers of large corporations. As the report points out (emphasis added):

The ‘fiduciary duty’ (financial responsibilities towards stakeholders) for local government pension funds is split between the fund beneficiaries (who would usually be the only ‘fiduciaries’), employers (mostly the local governments themselves) and local residents, whose taxes top up the pension pot. The duty owed to local residents means a wide body of people arguably should have some say in local government pensions.

Yet despite all this, Carney U-turned, leading the financial capture of COP26 in Glasgow:

One desperate solution to the problem of a waning shale industry in the US was to export fracked gas abroad. With the first deliveries of fracked ethane gas arriving at Grangemouth, INEOS has us all believing that this will be the great panacea for the shale gas revolution. But This article from Desmog tells a very different story. The problem being that everyone else was suffering from low prices:

LNG prices hit 18-year lows this month, in part due to collapsing demand from China and other Asian countries for commodities and in part because other countries have also invested heavily in building export facilities at the same time as the U.S.

The article continues:

And since the process of liquefying the natural gas and shipping it carries additional costs — potentially enough to eat through all of the higher price that LNG commands in some international markets — that’s bad news for the shale drilling industry, already under enormous financial pressure from the collapse of oil prices by roughly two thirds since 2014.

Since the start of last year, over 50 North American oil and gas producers have filed for bankruptcy. But the oil and gas has continued to flow (in part because even when drillers go bankrupt, their existing wells are usually left in production by their creditors).

Those who expect that LNG exports will reverse the fortunes of shale gas drillers may be in for a rude awakening. “The low and volatile energy price environment is forcing developers to tighten belts and we can expect more proposed projects to delay investment decisions,” James Taverner, a Tokyo-based analyst at IHS Inc., told Bloomberg. “There are far more LNG projects competing to go ahead than the market can absorb.”

In January 2018, I authored a detailed report on shale gas and particularly INEOS’ involvement.

With the war in Ukraine, global prices have rocketed. But as the old saying goes, all good things eventually come to an end. Ultimately the shale gas industry will decline as the very expensive infrastructure that accommodates an export/import market will once again become volatile. And the only response from players will be lots of hype and casino policies, that just like the coal industry could lead to collapse and the pressing issue of stranded assets. The question is, why?

The Smith School of Enterprise and the Environment, Oxford University, has been conducting research into stranded assets. It offers a straight forward definition and notes a lack of understanding:

Stranded assets are assets that have suffered from unanticipated or premature write-downs, devaluations, or conversion to liabilities and they can be caused by a variety of risks. Increasingly risk factors related to the environment are stranding assets and this trend is accelerating, potentially representing a discontinuity able to profoundly alter asset values across a wide range of sectors.

Yet environment-related risks that could strand assets are poorly understood and regularly mispriced, resulting in an over-exposure to such risks throughout our financial and economic systems.

This leads to a stranded assets trap:

A hypothesised vicious cycle where a company cannot generate sufficient free cash flow from its core activities (as the sector or market segment in question is in structural decline due to environment-related risk factors) to finance diversification using internal capital or capital from investors. The more the company invests in its core activities to improve diminishing margins in the structurally declining sector or market segment, the less financial capacity it will have to diversify into other areas and the less plausible diversification looks as a strategy to external investors. As a result, the company continues to focus on core activities to improve diminishing margins, which in turn makes it harder to finance diversification, continuing the cycle.

And all this could lead to a widespread market collapse across the length and breadth of the fossil fuel industry. The urgency to divest from fossil fuels and reinvest in safe infrastructure could not be more pressing.

The tremors from the coal collapse running through our pension funds and other investments, resulted in the UK Government’s manic obsession of rolling out a shale gas industry in the UK, then hitting the brick wall of hard reality, whilst still investing in white elephants such as Hinckley Point.

As for the problem of stranded assets, there’s an ongoing scam that helps to deal with that particular problem. It ties into the investor-state dispute settlement (ISDS) mechanisms that has become prevalent in trade deals. This report from the International Institute for Environment and Development (iied), published in 2020, Raising the cost of climate action? Investor-state dispute settlement and compensation for stranded fossil fuel assets, details how ISDS is providing a safety net for the fossil fuel industry, at the expense of tax payers.

The report outlines how the COVID pandemic hit the industry hard, but with a distinctive rebound following easing of lockdowns. In particular it had the effect of putting the final nail in the coal industries coffin. The report notes that:

the pandemic has starkly illustrated that emissions reductions on the scale required will not occur without sustained government action to facilitate a fundamental transition away from fossil fuel production and consumption, towards low-carbon energy sources.

But there’s a catch. With a raft of treaties and trade agreements:

This enables foreign investors to sue states over conduct that they believe breaches international investment protection rules… .

Foreign investors may resort to ISDS to sue states over measures to phase out fossil fuels. Even in the absence of legal proceedings, the explicit or implicit threat of recourse to ISDS can enhance the position of businesses in negotiations with states. As a result, more public funds may be spent on compensating the fossil fuel sector than would otherwise be the case, partly because — as we will see in this report — tribunals have often awarded large compensation amounts. This can make it more costly for states to take energy transition measures.

There’s a stark warning about what’s at stake. Already we are getting close to exceeding the carbon budget, as outlined in an IPCC Special report (2018). According to this, the budget will be breached in less than 12 years. But there’s no sign of any turn around as the fossil fuel industry continues to invest in infrastructure - mostly refineries - ‘with US$52 billion going into the construction of new refineries in 2019 alone.’ This would generate overcapacity in the future:

Globally, the value of stranded assets could be as much as US$1.8 trillion for the power sector alone. The estimated value of stranded assets is lower under a scenario where ambitious action on climate change is taken sooner, because such action would deter further investments in carbon-intensive assets that would eventually have to be stranded. Meanwhile, the estimated value of stranded assets in the upstream oil and gas industry is US$3–7 trillion.

Yet Governments’ hands are tied, even if they refuse to engage with the process:

proceedings can continue even if the government does not take part. Widely ratified multilateral treaties such as the New York and Washington Conventions facilitate the enforcement of pecuniary awards. These features mean that ISDS has legal bite against non-complying states.

…Recent years have witnessed consistently high numbers of new cases. The boom has been fuelled by:

investors’ direct access to international redress, without needing to exhaust local remedies first;

broad interpretations of the protections provided to foreign investors, made by ad hoc tribunals; and

large compensation awards that sustain an international industry of adjudicators, lawyers and financiers.

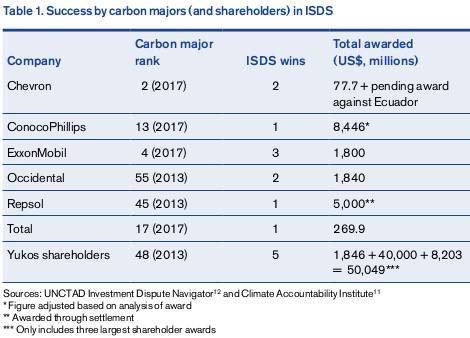

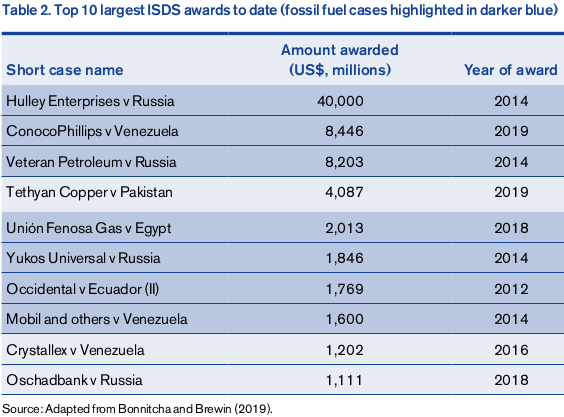

And as the report particularly notes that, ‘Company shares are a protected form of investment under most treaties with ISDS’. Around 54% known ISDS cases went through the Energy Charter Treaty (ECT), which is the most frequently invoked treaty in history. This was covered in detail in the previous article (see above).

The following table from the report paints a concerning picture:

And as this table shows, most of the biggest awards have gone to fossil fuel companies:

The bottom line is that is that if Government’s actually start engaging in saving the planet, then we can expect a surge in cases under ISDN. Or as the report puts it:

even cases that do not revolve around environmental measures can have indirect reverberations for measures to tackle climate change. Providing the industry with what is, in effect, a form of free risk insurance is equivalent to a subsidy.

Or to put it another way, we’re damned if we do and damned if we don’t. This then creates a situation of ‘regulatory chill’, whereby ‘states will fail to take public interest action as a result of concerns about ISDS’. It’s worth noting here that the US has never lost an ISDS case.

The report sums up:

Even with the current state of the empirical evidence, ISDS can have far-reaching repercussions for decisions about the low-carbon energy transition — not only because businesses may initiate ISDS disputes, but also because of the under-the-radar processes that ISDS can stimulate, including various forms of regulatory chill and negotiations in the shadow of ISDS. The large amounts of money at stake can make it more costly, and thus more difficult, for states to take the measures necessary to keep warming below 1.5°C. It can also create a disincentive for businesses to divest from fossil fuel assets.

A paper published in Science in May 2022, Investor-state disputes threaten the global green energy transition, elaborates on the issues raised in the above report. It notes how ISDS was raised by the IPCC in its Working Group 3 assessment report (2022), even if it does only cover a few lines (CH, 14.5.2.2):

Despite improvements in the international governance of energy, it still appears that a great deal of this is still concerned with promoting further development of fossil fuels. One aspect of this is the development of international legal norms. A large number of bilateral and multilateral agreements, including the 1994 Energy Charter Treaty, include provisions for using a system of investor-state dispute settlement (ISDS) designed to protect the interests of investors in energy projects from national policies that could lead their assets to be stranded. Numerous scholars have pointed to ISDS being able to be used by fossil-fuel companies to block national legislation aimed at phasing out the use of their assets.

The paper urges Governments take actions preventing fossil fuel investors from accessing ISDS. Given that under the carbon budget, ‘nearly 60% of oil and fossil methane gas reserves and 90% of coal reserves cannot be extracted,’ its clear that many existing operations are unviable. But as I covered previously, the launch of the Beyond Oil and Gas Alliance (BOGA) at COP26 represents an important development. But despite this and with the real threat of arbitration, which could be devastating for low income states:

despite a growing body of research, there is a lack of understanding on the part of many states that the treaties do not live up to their purported benefit of facilitating investment.

And:

asset valuation is complicated by the volatility of oil prices, which are highly sensitive to exogenous shocks such as the pandemic and the war in Ukraine.

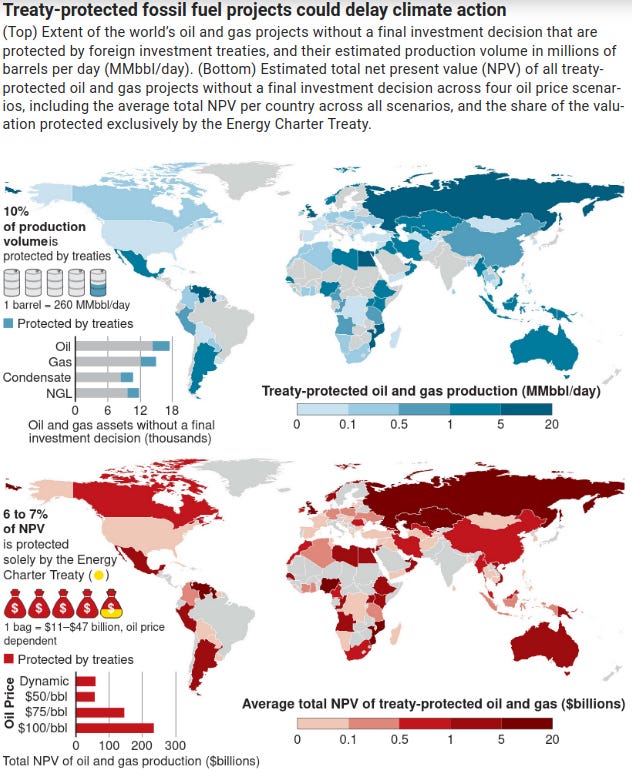

The following infographic shows treaty protection relative to production.

The paper cites possible remedies for dealing with the problems of ISDS. It notes work being conducted by the Organisation for Economic Co-operation and Development (OECD). According to the OECD, it is working on future investment treaties that will take account of the climate crisis. Apparently this includes:

ensuring treaties contribute to sustainable development and do not hamper legitimate regulation in the public interest

providing a framework to support market openness, facilitate investment and promote responsible business conduct

considering a more flexible range of procedures and remedies when treaties are implemented

examining which issues may be best addressed in treaties, and which may be better suited for regulation through domestic law, international guidance or other tools.

This all follows a consultation that took place in 2020, which then culminated in a conference in May 2022. As this is work in progress, it remains to be seen whether something constructive emerges.

How does all this tie into shale gas expansion through LNG? The Global Gas & Oil Network has a resource that maps the prevalence of oil and gas infrastructure around the globe. The Europe Gas Tracker:

covers gas pipelines, LNG terminals, gas-fired power plants, and gas extraction sites. The map and underlying data are updated every year in February, and each project has a dedicated wiki page on GEM.wiki that provides extensive detail on the project, such as the project’s status, capacity, cost and ownership.

The interactive map can be used to highlight infrastructure of interest. Here is a screenshot showing the current state of LNG terminals and shipping routes:

The rolling out of LNG infrastructure is loaded with uncertainty though. Two reports, published in March 2022, from Global Energy Monitor (GEM) outlines this conundrum. The first outlines the global expansion of gas and how this conflicts with climate commitments. It estimates an increase of global gas energy output of 615 GW at a cost of US$509 billion. In particular:

when European policy makers are working to decrease the continent’s

dependency on imported gas, Europe is planning over 65 GW of new gas-fired capacity.

With renewables now highly competitive, this presents a stranded asset and investment risk. This is elaborated upon in the second report.

The rollout of LNG from the US is dependent on export terminals. The map above shows Texas as currently the main export hub. The report notes that ‘21 LNG export terminals that are currently proposed in the United States’, have not ‘yet reached a final investment decision (FID).’ The proposed terminals have received limited interest from investors. This due to a combination of factors that includes; climate concerns, volatile markets and the untenability of fossil fuels in an increasingly competitive market with renewables and a shift in regulatory policies. Even with the war in Ukraine, rolling out gas infrastructure is a long term issue. With increasing pressure for divestment in fossil fuels and competition from renewables and energy efficiency, the tide will ultimately shift.

Reinvestment

We are facing high youth unemployment, housing shortfalls, increasing inequalities, significant cuts to health and education services, and growing risks associated with climate change, worsened by a lack of investment in low carbon infrastructure and cuts to renewable energy support.

If you are going to divest from fossil fuels, where do you put the money instead? A report from Platform Reinvesting Pensions: From fossil fuel divestment to reinvestment in the new economy, attempts to answer that question.

The report notes:

Just when civic leadership is needed most, austerity cuts have compromised local government’s capacity to respond in a joined up fashion. Since the 2010 Spending Review, funding to local government in the form of grants will have been cut by approximately 64%. In order to cope, councils have slashed staff numbers, shedding long-term strategic capacity in areas including planning, policy and environment. Cuts to funding have gone so far that the National Audit Office has warned 50% of councils may fail by 2020 and DCLG [Department for Communities and Local Government], the department responsible for managing them, has no way of tracking their financial health.

This paints a dark picture for our communities. Yet there appeared to be no shortage of funds allocated for the purpose of ‘going all out for shale’ or for setting aside an eye watering £200 billion on Trident.

At the same time, Local pension funds have been investing up to £14 billion into fossil fuels. With 80% of known reserves needing to stay in the ground in order to avoid catastrophic climate change, this represents a major risk for these funds. Divestment on the other hand could provide a boost for local economies:

Pensions can be harnessed to drive the energy transition, create local jobs and support local innovation. Pensions can be more effectively put to work by creating and retaining value in local economies, while establishing new community ownership models. The longterm nature of pension investments allows for the support of infrastructure essential in reducing inequality and meeting climate commitments.

The report sums up:

By divesting and reinvesting £14 billion into renewable energy, public transport and social housing, local government could create jobs, boost local economies and future proof against climate change while protecting pensions.

An underlying obligation for pension funds is Fiduciary duty. This is a legal obligation that requires trustees to act in the best interest of their members. Climate change could challenge pension funds approach to fiduciary duty. The report explains:

Christopher McCall QC a pre-eminent legal expert on fiduciary duty raised the prospect that charities may be legally required to re-evaluate their approach to carbon intensive investments. Helena Morrissey, CEO of Newton and chairman of the Investment Management Association, recently warned that the impact of climate policy is still not high enough on the agenda of most investment managers and has warned her peers that “We slept walked into the financial crisis and we have no excuse for sleepwalking into a climate crisis.”

The report notes a statement from Environmental Law firm ClientEarth, citing a legal perspective on the responsibilities of pension funds:

In the context of pension funds, it is now becoming widely accepted that climate change poses material financial risks to investment portfolios.

If the experts are correct, then our reading of the law strongly suggests that such risks should be mandatory considerations for pension funds when they are exercising their investment powers.

At ClientEarth, we believe there is sufficient and growing expert evidence to substantiate the view that climate risks should be mandatory considerations for trustees and fund managers when making investment decisions. Those who continue to ignore these risks, thereby jeopardising the pension pots of savers, may find themselves facing legal challenges.

But this isn’t so much a case of persuading funds to switch to more responsible investments, as they are already doing it. What is required is a scaling up of the process. As the report puts it, some ‘pension funds have already committed to responsible investment practices. These approaches have been tried and tested and can be adapted for divest:reinvest purposes.’

A strengthening of screening processes, following due process and due diligence would enable funds to expand their responsible portfolios. There are clear guidelines in place that could create an effective manageable framework that would allow funds to fulfill their obligations.

One such framework is the United Nations Principles of Responsible Investment (UNPRI), which defines responsible investment as:

…an approach to investment that explicitly acknowledges the relevance to the investor of environmental, social and governance factors, and of the long term health and stability of the market as a whole. It recognises that the generation of long term sustainable returns is dependent on stable, well functioning and well governed social, environmental and economic systems.

It is based on the following 6 principles:

We will incorporate environmental, social and governance (ESG) issues into investment analysis and decision-making processes.

We will be active owners and incorporate ESG issues into our ownership policies and practices.

We will seek appropriate disclosure on ESG issues by the entities in which we invest.

We will promote acceptance and implementation of the Principles within the investment industry.

We will work together to enhance our effectiveness in implementing the Principles.

We will each report on our activities and progress towards implementing the Principles.

Clearly the answer to the question posed above is to reinvest divested funds into sustainable infrastructure projects. Community energy is another area of importance. As the report points out:

In November 2015, the Scottish parliament’s Local Government and Regeneration Committee recommended that councils should maximise the opportunities presented through pension funds and City Deals to improve local infrastructure such as affordable housing. The report states that 5 out of 11 Scottish pension funds are already investing in infrastructure: Fife, Strathclyde, Borders, Falkirk, and Lothian.

There is also scope for inter-cooperation between different funds such as ‘Greater Manchester Pension Fund’s £500m infrastructure investment partnership with the London Pension Fund Authority, and the London pension funds’ new Collective Investment Vehicle.’

With regards to community energy, this is an area that has been expanding. But changes in the Feed in Tariff scheme and other reductions in funding has made it difficult for the market to expand further. However as the report points out:

RegenSW’s national Community Energy Accelerator programme suggests that the FIT cut threat has not caused community groups to stop work but, on the contrary, has galvanised them. With support, the community energy movement has been one of the strongest lobbyists for the renewable energy sector in this time of instability. Because they are socially motivated, community energy groups are already working hard to think about new business models and approaches which will allow them to achieve their goals. The costs of renewables globally are reducing rapidly and the sector will be viable in the UK without subsidy within a few years.

All that remains then is to persuade your pension fund to engage in responsible investment strategy. The report winds up with some pertinent suggestions:

Many local government pension funds are pursuing responsible investment strategies that can be adapted into a reinvestment strategy.

This report has identified a number of potential opportunities for reinvestment, from offshore wind funds (e.g. Green Investment Bank Offshore Wind Fund) and green bonds to social housing, commercial retrofitting (e.g. Low Carbon Work Place Fund) and renewables co-operatives.

Creation of specialist portfolios is an effective starter mechanism to facilitate low carbon and socially positive investments. Those local government pension funds that haven’t already created new portfolios specifically for renewable energy, social housing, and low carbon infrastructure should do so. A proportion of divested funds should be used for investment into the new portfolios. Since divestment is a phased process, different investment strategies for the specialist portfolios can be tested and adjusted over time.

Funds that already have such portfolios can expand the portfolios’ capacity using divested funds.

Both new and existing specialist portfolios should earmark a percentage of the total portfolio for investment into projects that have clear democratic governance structures to facilitate the democratisation of the low carbon economy.

As a short to medium term option, pension funds can invest into low carbon index tracker funds.

Community energy investment is one way of elbowing out UGE. One initiative involves Lancashire county council’s pension fund, pertinent given the area’s involvement with the campaign against UGE.

This article explores the background:

Lancashire county council’s pension fund has invested £12m in the UK’s first community-owned solar development in South Oxfordshire.

Westmill, which is also believed to be the world’s largest solar co-operative, consists of 21,000 panels that generate enough electricity to power 1,400 homes.

The project has agreed a deal with the pension fund that sees it receive a £12m bond — with Lancashire county council receiving interest on its investment over the 23-and-a-half year period.

The project may be outside the geographical remit of the fund, but it does demonstrate the scope and prospects for wide cooperation between pension funds around the UK and community energy projects.

And just to round up the argument, this article from Alternet sums up the global momentum that has been gaining ground:

Investors who have dumped holdings in fossil fuel companies have outperformed those that remain invested in coal, oil and gas over the past five years according to analysis by the world’s leading stock market index company.

MSCI, which runs global indices used by more than 6,000 pension and hedge funds, found that investors who divested from fossil fuel companies would have earned an average return of 13% a year since 2010, compared to the 11.8%-a-year return earned by conventional investors.

What is required is a grass roots initiative in order to achieve a paradigm shift in how we utilise our energy resources. Another paper from Platform uses the NHS as an example of how during the post war period, the public service was rolled out, revolutionising health care in the UK.

Energy beyond neoliberalism outlines a viewpoint that we need ‘energy alternatives that break with the foundational assumptions of the neoliberal order.’

Platform homes in on the issue:

A century-long strategic alliance between fossil fuel corporations and Western governments has fostered an energy system that has been structured by imperial, extractivist and then neoliberal power. Global neoliberal extractivism — based on the exploitation of non-renewable natural resources — is now trying to solve the dwindling of easily accessible oil reserves by violently pushing for new reserves to be exploited. Cue Arctic drilling, fracking and efforts to extract from beneath the pre-salt ultra-deep waters off Brazil. Once discovered and measured, geological deposits are represented as ‘proven reserves’ and they then become financial assets that are tradable and valued on the FTSE.

This process thrives on accumulation by dispossession: the expulsion of people from their land, the occupation of villages by soldiers, and the poisoning of groundwater. Military, diplomatic and financial support from states to corporations is key to its facilitation. The aim of Western states is to maintain imperial power by keeping their corporations in control of fuel flows. London is now a centre of both financial and energy imperialism.

The paper continues:

The whole relationship of society to energy needs to change. We need to shift power away from the entangled interests of finance and the big companies, and challenge the current monopolised energy system, so that these relationships can become intentional and active, so that energy consumers can become producers, distributors, owners, sharers and collective users of energy. We need to democratise energy. This means commoning resources, dispersing economic power and ending dependence on the multinationals that exploit public resources for private profit.

Such initiatives have already unfolded in countries such as Denmark and Germany. In Scotland on the Isle of Eigg:

The Isle of Eigg in the inner Hebrides undertook a historic community buyout in 1997, and took control of their land. In 2008 the community switched on the island electrification project, making 24-hour power available for the first time to all residents and businesses on the island Hydro, wind and solar energy now contribute over 95 per cent of the island’s electricity demand. Eigg has also inspired energy co-operatives in England, ranging from places resisting fracking such as Balcombe and Barton Moss, to inner city estates in Hackney and Brixton.

Divestment and reinvestment is certainly important, with the aim of redistributing finance into the commons rather than a handful of elitist interests in the City. The paper sums up:

Pressure is building to divest from fossil fuels. But the ultimate aim is to divest from neoliberalism itself. By commoning finance, we could break the grip the City holds over the rest of Britain, and create the basis for a new financial architecture, dedicated to economic and energy democracy.

The fossil fuel sector and the financial sector are two corners of a neoliberal triangle that also links in to the military industrial complex. From Iraq to Libya, the Gaza strip to Yemen and now Ukraine, it all boils down to the control of fossil fuel resources by whatever force is deemed necessary.

The Campaign Against the Arms Trade highlights the triangle with its Arms to renewables campaign. The report Arms to Renewables: Work For The Future, focused on the transitioning of jobs from the defence sector to renewables. This is similar to the discourse surrounding the shift of the north sea oil and gas sector to renewables. The skills and capabilities of many workers in both arms and the north sea could be transferable to renewables.

The position of the UK Government though was apparently to lock the UK within a fossil fuel environment by rolling out an UGE industry whilst still relying on imports from oppressive regimes such as Saudi Arabia. As the report points out, the Middle East dominates global oil and gas production. This is also the region that most arms are shipped to:

The main focus of UK arms exports remains the Middle East, which, according to UKTI DSO, has been the source of 55% of UK arms export orders over the past decade. Deloitte suggests that “regional tensions” here will lead to increased purchases of equipment, and it is clear that military spending is increasing in a number of Middle East countries, not least Saudi Arabia, UAE and Oman. However, the extent to which arms spending is due to a military threat is debatable. A prime objective for Saudi Arabia appears to be maintaining the status quo of Gulf authoritarianism, as evidenced by its military intervention to help suppress democracy protests in Bahrain in 2011. It seems that the UK’s best prospect for increased arms exports is to some of the world’s most repressive regimes.

This ultimately leads to national security, which normally revolves around military security but in reality means securing a steady supply of fossil fuel sourced energy, using military oppression in the process. The report sums up what is required:

…we are proposing a fundamental review of the UK government’s approach to security, focused on the security and well-being of the population rather than on military and arms company interests. This would include a far greater emphasis on non-military “priority risks” in the government’s National Security Strategy as well as on the underlying drivers of insecurity such as climate change and competition over resources. It would mean the end of overseas military interventions, which damage both national and international stability and security. Billions of pounds would be saved each year by stopping the procurement and support of offensive military capabilities such as the nuclear arsenal, aircraft carriers and their F-35 fighter-bombers, and the air-to-air refuelling capacity.

And the greatest security threat of all is of course climate change:

The Oxford Research Group, which has a Sustainable Security programme, states that the loss of infrastructure, resource scarcity, and mass displacement of peoples will lead to “civil unrest, intercommunal violence and international instability”. This analysis also exists within the world’s militaries. The UK MoD has assessed climate change to be one of four “key drivers of change”. It says “Out to 2040, there are few convincing reasons to suggest that the world will become more peaceful. Pressure on resources, climate change, population increases and the changing distribution of power are likely to result in increased instability and likelihood of armed conflict.” It goes on to state, “Climate change will amplify existing social, political and resource stresses…. The effects of climate change are likely to dominate the global political agenda, especially in the developed world where it will represent an increasingly important single issue.”

As I reported in a previous article, this was an issue that the Pentagon had also explored. The conclusions were explicit, climate change is a major threat to the security and stability of our civilisation. Transitioning to extreme forms of unconventional energy extraction will only exacerbate the problem:

The importance of renewable energy in the UK’s future energy security appears to be well recognised by the UK public. A poll commissioned by RenewableUK in June 2014 asked respondents which of several choices should be the top priority for the UK to ensure future energy security. 48% selected “Investing more in renewable energy”. Second, with 15%, was “Building more nuclear reactors”. In addition to energy supply, shifting from imports to domestic production would provide wider security benefits: it would help ensure that the UK retains independence by avoiding reliance on individual suppliers, and also avoids the perceived need to intervene militarily to secure energy supplies.

The conclusion is clear then. If overall security is desired, divestment from both fossil fuels and the military industrial complex is essential. This is something civil society needs to come to terms with.

There’s a direct relationship with fracking and the military. It revolves around Halliburton and former CEO Dick Cheney, US Vice President during the George W Bush presidency.

Cheney was the architect of the infamous Halliburton Loophole, which allowed the expansion of the shale gas industry across the US. Much of the infrastructure of the industry is underpinned by Halliburton.

But in 2003, Cheney and his former employer played a key role in another monumental event, namely the the illegal invasion of Iraq, which was characterised by an orgy of misinformation over alleged weapons of mass destruction.

As a CorpWatch article stated following the invasion:

As the first bombs rain down on Baghdad, CorpWatch has learned that thousands of employees of Halliburton, Vice President Dick Cheney’s former company, are working alongside US troops in Kuwait and Turkey under a package deal worth close to a billion dollars. According to US Army sources, they are building tent cities and providing logistical support for the war in Iraq in addition to other hot spots in the “war on terrorism.”

While recent news coverage has speculated on the post-war reconstruction gravy train that corporations like Halliburton stand to gain from, this latest information indicates that Halliburton is already profiting from war time contracts worth hundreds of millions of dollars.

From bombing Iraq to devastation across America from fracking and the Ukraine conflcit induced LNG boom, the inseparable relationship between ‘Big Oil’ and ‘Big Guns’ is unmistakable. And this relationship was underlined by Greenpeace in the run-up to the war:

Top oil analyst Dr. JJ Traynor of Deutsche Bank sees the US’s largest and undoubtedly most politically influential company, ExxonMobil, as being in “pole position” to take full advantage of a regime change in Iraq. (Find out more from www.stopesso.com.)

ExxonMobil has worked hard to ensure demand for oil by pressuring the US government into abandoning its commitments to the Kyoto Protocol on global warming. During the 2000 election cycle, ExxonMobil gave $1,375,250 to political campaigns — second only to Enron among oil and gas company campaign contributions. Of this total, 89 percent went to Republican candidates. By undermining efforts to reduce greenhouse gas emissions, ExxonMobil prolongs US’s oil dependence and prolongs its entanglements with often politically unstable oil producing countries.

However, unlike its French, Russian and Chinese counterparts, ExxonMobil, the world’s biggest oil company, has had to stay away from Iraq due to the US political situation in the last ten years. Exxon previously owned 25 percent of Iraqi oil fields and a new war with Iraq would again open up access to Iraq’s large oil reserves.

And lets not forget the other corner of the triangle — ‘Big Money’. Eventually the triangle resembles more like a vicious circle, the same circle referred to in the Smith School definition above. A circle that involves Big Money pumping more dollars into Big Oil and Big Guns, with each reinforcing the other.

As conventional sources of fossil fuels run out, the tendency with be to transition to extreme energy — fracking, tar sands, deep water drilling, etc. All this will exacerbate climate change, and as the shit hits the fan, those holding the reins of power will do anything to hold on to it. You only need to look at the Pentagon and MOD reports on climate change to get the message. Breaking the circle is a duty, not merely an option. If not, then a catastrophic collision is inevitable. Not only will this knock out the fossil fuel dinosaur, it will take out everything else as well.